Verdict: FactCheck concludes that Irakli Kobakhidze’s statement is MOSTLY FALSE.

Resume: In 2012, the total revenues in the state budget amounted to GEL 7,115 million. In accordance with the planned amount of budget revenues for 2018, the total revenues comprise GEL 10,314 million which constitutes a 45% growth as compared to 2012. However, equating budget revenues and the population’s taxable income is incorrect because budget revenues also include those funds which are not related to the taxable income of individuals such as, for instance, grants. In addition, only emphasising “citizens’ income” whilst speaking about budget revenues is also incorrect because individuals are not the only taxpayers.

Revenues from income taxes were GEL 1,636 million in 2012 and will reach GEL 2,780 million according to the plan for 2018 which constitutes a 69% growth. However, this method does not offer the possibility for making a precise judgment because the amount of tax collection increases not only because of the growth in taxable income. There could be several different reasons behind the growth of tax collection such as an improvement in administering taxes, reducing the number of informal contracts, etc. On the other hand, this method does not take changes in GEL purchasing power (inflation) into account. As of January-August 2018, the inflation rate increased by nearly 19.4% as compared to 2012.

In his statement, Irakli Kobakhidze tries to underline the growing prosperity of hired workers who pay income tax. In terms of taxed income, taxed directly by an employer, GEL 842 million was accumulated in the state budget as of January-August 2012 whilst this figure was GEL 1.773 billion in the same period of 2018. The growth rate was 110% although this figure is not fully related to income growth. Here, improvements in administering taxes, inflation and other factors again need to be taken into account.

Budget revenues are nominal figures and any discussion about a population’s income in different periods of time based only on these figures cannot depict the reality if we do not look at the increase in prices. For instance, GEL purchasing power was higher in 2012 as compared to 2018. Therefore, it is more appropriate to analyse real figures which are adjusted for inflation. The real average salary of the first quarter of 2018 increased by 33% as compared to the same period of 2012.

Analysis

On 25 September 2018, on air on the talk show Reaktsia, the Speaker of the Parliament of Georgia, Irakli Kobakhidze, stated: As compared to 2012, budget revenues have increased by 50%. This means that the taxable income of Georgian citizens increased by 50%.”

Mr Kobakhidze named these figures to illustrate the growing prosperity of hired workers who pay income taxes.

In 2012, the actual revenues received from income tax amounted to GEL 1,636.356 thousand whilst the total revenues amounted to GEL 7,115,329. In accordance with the plan for 2018, revenues from tax income constitute GEL 2,780,000 whilst the total revenues will reach GEL 10,314,248. Therefore, the revenues from income tax increased by 69% and total budget revenues increased by 45%.

It is not appropriate to equate budget revenues and the population’s taxable income. Budget revenues consist of taxes, grants and other incomes of different classifications. Therefore, budget revenues include funds which are not related to the taxable income of individuals. The budget line for grants clearly illustrates this case.

Table 1: Tax Consolidated Revenues in the State Budget in 2012 (Actual Amount) and 2018 (Planned Amount) GEL Thousand

Source: Ministry of Finance of Georgia

Multiple factors affect the increase or decrease in any the aforementioned budget lines. For instance, increased excise tax on fuel and tobacco would naturally increase revenues from excise tax whilst launching the so-called Estonian Model would decrease revenues from profit tax, etc.

Perhaps an imprecise but theoretically more relevant indirect indicator for the changes in a population’s taxable income could be the changes in budget funds accumulated in the form of income tax itself. However, measuring general prosperity based on money collected as income tax has a certain limitation; namely, the tax collection figure does not increase only because of the growth of taxable income, on the one hand. There could several different reasons behind an increase in tax collection such as improvements in administering taxes, a decreased number of informal deals, etc. On the other hand, this does not take the changes in GEL purchasing power (inflation) into account.

As of January-August 2018, the inflation rate increased by 19.4% as compared to the same period of 2012. Without taking a look at the increased level of prices, any discussion about nominal revenues does not give a precise picture because budget revenues are indeed nominal figures. For instance, GEL had a higher purchasing power in 2012 as compared to 2016 and less purchasing power as compared to 2002. Therefore, it is more appropriate to analyse real figures adjusted for inflation.

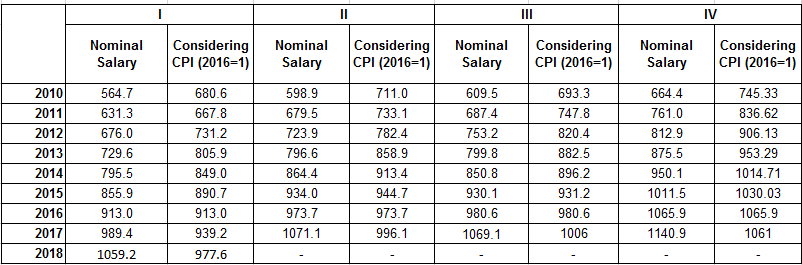

Table 2: Hired Workers’ Average Monthly Salary (GEL)

Source: National Statistics Office of Georgia

As illustrated in Table 2, the real average salary (GEL 977) of the first quarter of 2018 increased by 33% as compared to the real average salary (GEL 731) of the same period of 2012.

At the same time, Irakli Kobakhidze speaks about “citizens’ incomes” in the context of budget revenues. Therefore, it is important to clarify that in accordance with the Tax Code of Georgia, an income tax payer is an individual (both resident[1] and non-resident) who has received income from a source in the country for a certain period of time. Therefore, income tax is paid by resident or non-resident individuals who might not be Georgian nationals. Consequently, the change in tax revenues illustrates a possible trend of changes in taxpayer incomes and not in citizens’ incomes.

[1] A resident is an individual who actually resides on the territory of Georgia for more than 182 days in a 12-month period within one tax year. A resident is also an individual who has been abroad during a tax year whilst employed in Georgia’s public service.

Source: National Statistics Office of Georgia

As illustrated in Table 2, the real average salary (GEL 977) of the first quarter of 2018 increased by 33% as compared to the real average salary (GEL 731) of the same period of 2012.

At the same time, Irakli Kobakhidze speaks about “citizens’ incomes” in the context of budget revenues. Therefore, it is important to clarify that in accordance with the Tax Code of Georgia, an income tax payer is an individual (both resident[1] and non-resident) who has received income from a source in the country for a certain period of time. Therefore, income tax is paid by resident or non-resident individuals who might not be Georgian nationals. Consequently, the change in tax revenues illustrates a possible trend of changes in taxpayer incomes and not in citizens’ incomes.

[1] A resident is an individual who actually resides on the territory of Georgia for more than 182 days in a 12-month period within one tax year. A resident is also an individual who has been abroad during a tax year whilst employed in Georgia’s public service.

| 2012 Actual Amount | 2018 Planned Amount | |

| Budget Revenues | 7,115,329.30 | 10,314,248.00 |

| Tax Revenues | 6,311,078.10 | 9,490,000.00 |

| Income Tax | 1,636,356.00 | 2,780,000.00 |

| Profit Tax | 850,995.00 | 630,000.00 |

| Value Added Tax | 3,040,331.80 | 4,400,000.00 |

| Excise Tax | 659,606.10 | 1,450,000.00 |

| Import Tax | 90,079.00 | 60,000.00 |

| Other Taxes | 33,710.10 | 170,000.00 |

Source: National Statistics Office of Georgia

As illustrated in Table 2, the real average salary (GEL 977) of the first quarter of 2018 increased by 33% as compared to the real average salary (GEL 731) of the same period of 2012.

At the same time, Irakli Kobakhidze speaks about “citizens’ incomes” in the context of budget revenues. Therefore, it is important to clarify that in accordance with the Tax Code of Georgia, an income tax payer is an individual (both resident[1] and non-resident) who has received income from a source in the country for a certain period of time. Therefore, income tax is paid by resident or non-resident individuals who might not be Georgian nationals. Consequently, the change in tax revenues illustrates a possible trend of changes in taxpayer incomes and not in citizens’ incomes.

[1] A resident is an individual who actually resides on the territory of Georgia for more than 182 days in a 12-month period within one tax year. A resident is also an individual who has been abroad during a tax year whilst employed in Georgia’s public service.

Tags: