Nodar Ebanoidze, Member of the Georgian Dream Faction-Republicans, stated at the plenary session held on 26 June 2013: “Neither the regulation, nor the law or regulatory act determines rights and duties, authorities or other requirements of the head auditor, senior auditor, supervisor auditor, assistant auditor and auditor intern.”

FactCheck decided to determine whether or not Nodar Ebanoidze’s statement was true.

Since 1 July 2012 the Supreme Audit Institution of Georgia was re-established as the State Audit Office of Georgia (SAOG).The mandate of the State Audit Office of Georgia is laid down in Article 97 of the Constitution of Georgia. The status, mandate and procedures of the State Audit Office are guaranteed by the Law of Georgia on State Audit Office.

The Law determines that the general goals of the activity of the State Audit Office shall be: to promote efficient and effective public spending, to protect national wealth, property of state of autonomous republics and local (municipal) entities and to improve management of public finances.

The State Audit Office of Georgia conducts financial monitoring of the political parties within the competences defined in the Organic Law of Georgia on the Election Code of Georgia and the Political Union of Citizens.

The State Audit Office shall be independent in its activities. Any interference in or/and control of its activities and request for reports related to its activities shall be inadmissible, if this is not explicitly provided for by the law. Any political pressure as well any other actions that may encroach on its independence shall be prohibited.

Rules of Procedure of the State Audit Office determines the rules of operation of the SAOG, its structure, the functions of its structural units, terms and rules of audit preparation and conducting, rules of execution of the mandate, management reporting and other organisational issues of internal activities.

The Code of Ethics of the Auditors of the State Audit Office represents a set of general principles defining the rules of conduct for their capacity as SAOG auditors.

As previously mentioned, the status, mandate and procedures of the State Audit Office are guaranteed by the Law of Georgia on the State Audit Office which also includes the rights and responsibilities of the auditors of the State Audit Office.

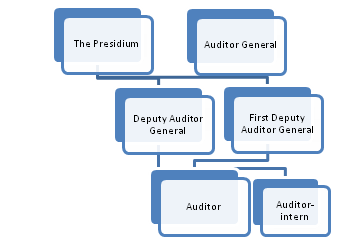

The structure of the State Audit Office is the following:

Article 13 under the Law of Georgia on the State Audit Office and Chapter 4 under the Rules of Procedure of the State Audit Office determine the rights and duties of the Presidium.

Article 9 and Article 10 under the Law of Georgia on the State Audit Office and Chapter 2 under the Rules of Procedure of the State Audit Office respectively determine the rights and duties of the Auditor General.

Paragraphs 5,6 and 7 under the Rules of Procedure of the State Audit Office and Article 12 under the Law of Georgia on State Audit Office determine rights and duties of the Deputies Auditor General ( First Deputy, Deputy).

According to Article 20 under the Law of Georgia on the State Audit Office, audit can be conducted by the Auditor and Auditor Intern. The same Article determines their rights and duties in the process of auditing; however, full authorities are determined neither by the Law nor the Rules of Procedure.

The Law of Georgia on the State Audit Office and the Rules of Procedure of the State Audit Office do not determine rights and duties of those persons conducting auditing, such as the Senior Auditor, Supervisor Auditor or Assistant Auditor.

FactCheck wondered whether or not such positions in the State Audit Office actually exist. For this purpose, we contacted the Legal Department at the State Audit Office to determine the following issues:

Article 13 under the Law of Georgia on the State Audit Office and Chapter 4 under the Rules of Procedure of the State Audit Office determine the rights and duties of the Presidium.

Article 9 and Article 10 under the Law of Georgia on the State Audit Office and Chapter 2 under the Rules of Procedure of the State Audit Office respectively determine the rights and duties of the Auditor General.

Paragraphs 5,6 and 7 under the Rules of Procedure of the State Audit Office and Article 12 under the Law of Georgia on State Audit Office determine rights and duties of the Deputies Auditor General ( First Deputy, Deputy).

According to Article 20 under the Law of Georgia on the State Audit Office, audit can be conducted by the Auditor and Auditor Intern. The same Article determines their rights and duties in the process of auditing; however, full authorities are determined neither by the Law nor the Rules of Procedure.

The Law of Georgia on the State Audit Office and the Rules of Procedure of the State Audit Office do not determine rights and duties of those persons conducting auditing, such as the Senior Auditor, Supervisor Auditor or Assistant Auditor.

FactCheck wondered whether or not such positions in the State Audit Office actually exist. For this purpose, we contacted the Legal Department at the State Audit Office to determine the following issues:

Article 13 under the Law of Georgia on the State Audit Office and Chapter 4 under the Rules of Procedure of the State Audit Office determine the rights and duties of the Presidium.

Article 9 and Article 10 under the Law of Georgia on the State Audit Office and Chapter 2 under the Rules of Procedure of the State Audit Office respectively determine the rights and duties of the Auditor General.

Paragraphs 5,6 and 7 under the Rules of Procedure of the State Audit Office and Article 12 under the Law of Georgia on State Audit Office determine rights and duties of the Deputies Auditor General ( First Deputy, Deputy).

According to Article 20 under the Law of Georgia on the State Audit Office, audit can be conducted by the Auditor and Auditor Intern. The same Article determines their rights and duties in the process of auditing; however, full authorities are determined neither by the Law nor the Rules of Procedure.

The Law of Georgia on the State Audit Office and the Rules of Procedure of the State Audit Office do not determine rights and duties of those persons conducting auditing, such as the Senior Auditor, Supervisor Auditor or Assistant Auditor.

FactCheck wondered whether or not such positions in the State Audit Office actually exist. For this purpose, we contacted the Legal Department at the State Audit Office to determine the following issues:

- Is there a State Audit Office position of those persons carrying out auditing duties such Senior Auditor, Supervisor Auditor and Auditor Intern?

- What are the rights and duties of people holding these positions and which legislation regulates their activities?

- Are the rights and duties of the abovementioned persons different?