Resume: A sharp depreciation of GEL against USD, stipulated by a combination of internal and external factors (see FactCheck’s article), started in late 2014. As of today, GEL has lost 70% of its value against USD as compared to 2014 (the 50% depreciation mentioned by the President of the National Bank of Georgia refers to the 2014-2015 figure and is correct) and 10% as compared to the beginning of 2020. In spite of the sharp depreciation of the national currency, annual inflation in 2014-2015 did not exceed the targeted figure and reached 2% and 4.9% in 2014 and 2015, respectively. However, in the case of 2015, Koba Gvenetadze’s statement, despite being contextually correct, does contain a factual inaccuracy because inflation did not exceed 3% in that period.

The effect of the GEL exchange rate on inflation can be offset by other factors and the relation between these two economic parameters is indeed not direct which is manifested in different situations and in a different scale. However, all things being equal, a sharp and long-term depreciation of the GEL exchange rate does instigate significant inflationary pressure. This is proven by the response of the National Bank of Georgia (NBG) to the economic situation in the aftermath of the 20 June 2019 crisis (see FactCheck’s article) when the NGB resorted to monetary intervention and tightened monetary policy to cap inflation and stabilise the situation.

Analysis

The President of the National Bank of Georgia, Koba Gvenetadze, on air on TV Formula stated (from 19:00): “There is no such directly proportional relation between the GEL exchange rate and prices. If we take a look at 2014-2015 statistics in Georgia, although GEL depreciated by nearly 50%, inflation did not exceed 3%.”

The President of the National Bank of Georgia made this statement within the context of the coronavirus-induced crisis (see FactCheck’s article). In particular, in light of the sharp fall of oil prices, on the one hand, and the spread of the novel coronavirus, on the other hand, the world economy has entered a crisis. As a result, the GEL exchange rate against the USD fell to a historic low which gives rise to a myriad of negative expectations and questions among the population, including ones related to inflationary processes. The part of Koba Gvenetadze’s statement, where he speaks about the indirect relation between the currency exchange rate and inflation, does correspond to the reality. A drop in a currency exchange rate (depreciation) is not automatically reflected in inflation; that is, an increase in prices. The currency exchange rate is one of many factors that affect the level of prices.

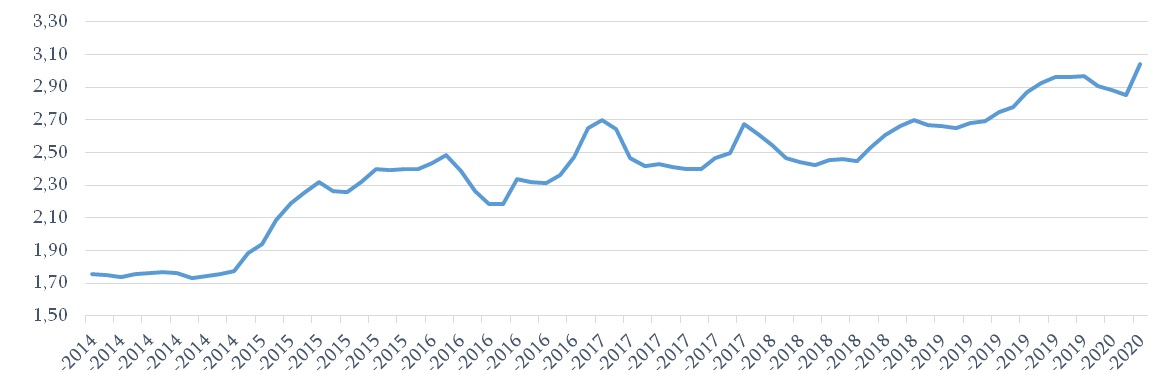

A sharp depreciation of GEL against USD, stipulated by a combination of internal and external factors (see FactCheck’s article), started in late 2014. As compared to 2014, GEL has lost 70% of its value against USD and 10% as compared to the beginning of 2020. As compared to 2014 (the 50% deprecation mentioned by the President of the National Bank of Georgia refers to the 2014-2015 figure and is correct). Of note is that after the initial and very sharp depreciation, GEL has been more or less stable.

Graph 1: GEL Average Monthly Exchange Rate Against USD in 2014-2020

Source: National Bank of Georgia

In spite of the aforementioned depreciation, annual inflation in 2014-2015 did not exceed the targeted figure and reached 2% and 4.9% in 2014 and 2015, respectively. However, in the case of 2015, the president of the National Bank of Georgia’s statement, despite being contextually correct, does contain a factual inaccuracy because inflation did not exceed 3% in that period.

Table 1: Actual and Targeted Inflation Figures in 2014-2019

|

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|

|

December as compared to previous December |

2.0 |

4.9 |

1.8 |

6.7 |

1.5 |

7.0 |

|

Targeted Inflation |

6.0 |

5.0 |

5.0 |

4.0 |

3.0 |

3.0 |

Source: National Statistics Office of Georgia

The effect of the GEL exchange rate on inflation can be offset by other factors. However, all things being equal, a sharp and long-term depreciation of the GEL exchange rate does instigate significant inflationary pressure. This is proven by the response of the National Bank of Georgia to the economic situation in the aftermath of the 20 June 2019 crisis (see FactCheck’s article). In late July 2019, USD value in commercial banks reached GEL 3 which the public considered to be the psychological threshold of the national currency’s “resilience.” To stabilise the situation, the National Bank of Georgia resorted to monetary intervention and indicated its readiness to further tighten monetary policy, if necessary. This was a notable occurrence since it was the first time when the National Bank assessed the depreciation of the GEL exchange rate as a danger of rising inflation.