Resume: The tax burden measurement indicator, to which Ivane Machavariani is referring and according to which Georgia is ranked 3rd in the world, is the total tax payable[1] as the share of gross profit which is one of the components of the World Bank’s Ease of Doing Business ranking. Therefore, referring to this indicator in regard to changes in taxes/incentivising business is irrelevant since it does not include indirect taxes.[2] The tax revenues to GDP ratio is generally used to measure the tax burden in a country and Georgia was ranked 35th in the world in 2017 based on this figure.

The example which runs counter to the claim of the Minister of Finance is the increased excise tax, including on petroleum products, which aimed to offset budget revenues after the introduction of the Estonian Model. Since 1 January 2017, excise fees on petroleum products have increased. The increased excise tax is a significant component of fuel price. Excise tax is an indirect tax which is eventually reflected in the final price of a commodity and the consumer will be the ultimate taxpayer. However, business naturally takes a hit as well because of the drop in demand. In addition, fuel is an intermediary product for many goods and services and an increase or decrease in fuel prices is directly linked with consumer prices; that is, inflation. In the past, the possibility of decreasing excise tax has been the subject of numerous political controversies. Bringing excise tax to its previous rate could have certain positive results and, on the other hand, given methodological reasons, an increase or decrease in excise tax cannot be reflected in Ivane Machavariani’s indicator. Therefore, the decision of the Minister of Finance to use this indicator as an argument is a manipulation of facts.

Analysis

In his speech as part of the Minister’s Hour before the Parliament of Georgia, the Minister of Finance, Ivane Machavariani, stated: “We are the number-three country in the world in terms of the tax burden. It would be impossible for us to provide incentives to business by further tax cuts or tax preferences.”

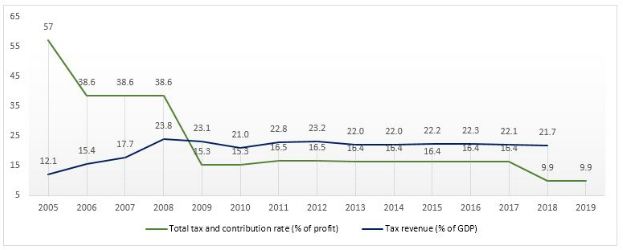

The indicator which measures the tax revenues to the gross domestic product (GDP) ratio is generally used to assess the tax burden in a country. In his statement, Ivane Machavariani refers to the total tax payable as the share of gross profit which is one of the components of the World Bank’s Ease of Doing Business ranking. Therefore, using this indicator in regard to changes in taxes/incentivising business is irrelevant since it does not cover indirect taxes. The tax burden dynamic in 2005-2019 is given in Graph 1.

Graph 1: Business Tax Burden and Tax Revenues to GDP Ratio in 2005-2019

Source: World Bank

The example which runs counter to the claim of the Minister of Finance is the increased excise tax, including on petroleum products, which aimed to offset budget revenues after the introduction of the Estonian Model.

Since 1 January 2017, excise fees on petroleum products have increased. The increased excise tax constitutes a significant component of fuel price. Excise tax is an indirect tax which is eventually reflected in the final price of a commodity and the consumer will be the ultimate taxpayer. However, business naturally takes a hit as well because of the drop in demand. Fuel is an intermediary product for many goods and services and an increase or decrease in fuel prices is directly linked with consumer prices; that is, inflation. A decrease in excise tax and a drop in fuel prices are reflected on the general price level. As a result, profit tax revenues in 2017 decreased by GEL 316 million as compared to 2016 whilst excise revenues in 2017 increased by GEL 365 million as compared to the previous year. The increased excise tax rate on petroleum products was followed by a one-off sharp hike in fuel prices. The price of petrol has increased by GEL 0.25, diesel by GEL 0.20-0.25 and gas by GEL 0.18. Therefore, bringing excise tax to its previous rate could have certain positive results and, on the other hand, given methodological reasons, an increase or decrease in excise tax cannot be reflected in Ivane Machavariani’s indicator. Therefore, the decision of the Minister of Finance to use this indicator as an argument is a manipulation of facts.

[1] Direct taxes – Taxes directly payable by enterprises (profit tax, property tax, etc.).

[1] The World Bank assessed 147 countries in 2017 and 62 countries in 2018. Therefore, discussing 2017’s conjecture would be more informative since Georgia’s indicator only marginally changed in 2018 as compared to 2017.

[2] Indirect Taxes – Taxes (VAT, excise, etc.) which are determined by raising prices on purchased goods or/and rendered services and which is ultimately paid by a consumer whilst making purchase of goods or/and services for a price which includes such tax.