The Minister of Finance of Georgia, Nodar Khaduri, commented upon the trend of a decrease in beer consumption and stated that it has nothing to do with the increase in the excise tax on beer. "You know that the excise tax increased by 20

tetri which increased revenues to the budget; however, our calculations confirm that the decrease in beer consumption was not caused by the increase in the excise tax," said Mr Khaduri.

FactCheck verified the accuracy of the Minister’s statement.

A law initiated by the Ministry of Finance of Georgia and requiring the increase of excise tax on tobacco products, malt beer, spirits and other alcoholic beverages was enacted on 1 January 2015. The excise tax on tobacco has already increased since 1 January (

FactCheck wrote about the issue earlier as well) whilst the regulation on malt beer, spirits and other alcoholic beverages was

enacted on 1 March 2015. Before the changes to the Tax Code of Georgia, excise tax on beer was 40

tetri per litre. As a result of the changes, however, the excise tax was increased by 50% (20

tetri) and amounted to 60

tetri.

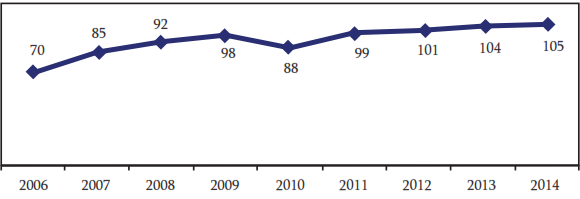

The beer market in Georgia grew by 45% from 2006 to 2014. It kept increasing every year with 2010 being the only exception (the excise tax on beer increased by 20

tetri in 2010 and amounted to 40

tetri). Beer consumption in Georgia varied from 100 to 105 million litres per year from 2011 to 2014. As of today, imported beer occupies a mere 3% of the market whilst the share of domestic beer is 97%.

Chart 1: Dynamics of Georgia’s Beer Market from 2006 to 2014 (Million Litres)

As already pointed out above, the excise tax on malt beer increased from March 2015. In order to find out whether or not these changes had any effect upon the beer market we reviewed the data from March to September 2015 and compared them to the data of the same period of the previous year.

Table 1: Beer Market Dynamics by Excise Tax Paid in 2014 and 2015 (from March to September)

| Year |

Month |

Beer Market (Million Litres) |

| 2014 |

March-September |

70.7 |

| 2015 |

March-September |

61.2 |

| Difference % |

|

-15% |

Source: Revenue Service of Georgia

As the table above makes clear, the beer market decreased by 15% from March to September 2015 as compared to the same period of the previous year (before the increasing of the excise tax).

It should be pointed out that according to the explanatory note of the 2015 State Budget of Georgia, the increase in the excise tax on malt beer, spirits and other alcoholic beverages would mobilise an additional GEL 30-40 million in the budget. The revenues received as a result of the growth of the excise tax on malt beer (first nine months of 2015) were GEL 5.9 million more than in the same period of the previous year which means that the growth was about 16.7%.

Table 2: Taxes Received from Beer Production in 2014 and 2015 (GEL Million)

| Tax |

2014 (9 Months) |

2015 (9 Months) |

Difference % |

| Excise Tax |

35.3 |

41.2 |

16.7% |

| VAT |

22 |

18.4 |

-16.4% |

| Income Tax |

4.6 |

4.7 |

1.2% |

Source: Revenue Service of Georgia

Another regulation had a negative effect upon the beer market. Article 171 of the Administrative Crime Code of Georgia was enacted in September 2014 which prohibited drinking beer in public places and the authority to determine the amount of the fine for this offence was given to the police as the body in charge of this regulation. As compared to the same period of the previous year (before the regulation was active), beer consumption decreased by 26%-28% in the two months following the enactment of Article 171 (October-November 2014).

Table 3: Beer Consumption in Litres from 2013 to 2014 (September to November)

| Month |

2013 |

2014 |

Difference |

Difference % |

| September |

8,032,585 |

8,192,056 |

159,471 |

2% |

| October |

5,828,914 |

4,285,105 |

-1,543,809 |

-26.5% |

| November |

4,467,156 |

3,568,586 |

-1,398,571 |

-28.2% |

Whilst studying this issue we contacted the Director of Corporate Issues at the Natakhtari Company, Nikoloz Khundzakishvili, and asked him to comment upon these legislative changes. According to his statement, increasing the excise tax on malt beer was a non-constructive step. "The increase in the excise tax on beer meant that production companies were forced to increase the prices as well. As a result, we have a decreased beer market. According to the data of the last nine months, we have a 19% drop which means that the state budget will not be able to get the fiscal effect it expected by making these legislative changes," said Mr Khundzakishvili.

As pointed out earlier in the article, the increase in the excise tax caused a drop in the market in 2010 as well. However, in the following years (before the excise tax was increased again), the market had a trend of increase. The future will show how the events will unfold in this case. It is a fact that the aforementioned legislative changes caused certain problems to one of the most successful fields of local production. The government will most certainly have to analyse which is greater – the positive fiscal effect from the increase in the excise tax or the negative effect for beer production companies owing to these changes.

Conclusion

From 1 March 2015, the amount of excise tax increased by 50% to 60 tetri per litre. Beer consumption dropped by 15% after March 2015 given the increased excise tax (it decreased by 19% according to the data of the first nine months of 2015).

The prohibition on drinking beer in public places also had an influence upon beer consumption. Beer consumption dropped by 26%-28% in the two months following the enactment of Article 171 as compared to the same period of the previous year. The decreased purchasing power caused by the depreciation of GEL is also added to this situation. Hence, the increase in the excise tax on malt beer was not the only reason for the drop in beer consumption but it definitely was the main reason for the shrinking of the beer market. In its

study, Transparency International Georgia also names the increased excise tax as a main reason for the decrease in Georgia’s beer market.

FactCheck concludes that Nodar Khaduri’s statement is

FALSE.