It has been five years since the adoption of the Law on Cumulative Pensions where beneficiaries are allowed to distribute their savings in high-risk, low-risk and medium-risk portfolios. The deadline to make these investment choices is 6 September 2023. Thereafter, changes to the investments are possible only after a 12-month period.

In order to distribute pension savings, citizens are required to submit an electronic statement from this personal savings page. They will need an ID-card reader or it will be possible to submit the statement at any branch of the Public Service Hall. If a person fails to submit a statement, the Pension Agency will automatically direct pension savings for those under 40 into high-risk or, in other words, rising assets. Persons between the ages of 40 and 50 will have their savings invested into medium-risk assets which are also called mixed assets and pension savings of people over 50 will be invested in low-risk or stable assets.

On 6 August 2018, the Law on Cumulative Pensions came into force and its principal element (making pension contributions) came into effect in January 2019. Employees under the age of 60 (55 in the case of women) were mandatorily switched to the plan, although people 40 years of age and above were allowed to leave the pension plan.

The system works on the 2+2+2 principle where 2% of a person’s taxable salary is paid by the employee, 2% is paid by the employer and 2% is paid by the state. If the employee's annual taxable salary is from GEL 24,000 to GEL 60,000, then the state adds 1% instead of 2% whilst the government contributes nothing if the salary exceeds GEL 60,000.

In 2019-2022, GEL 832 million GEL was spent on the co-financing of the cumulative pension system from the state budget. an additional GEL 310 million is planned for 2023.

Until August 2023, the savings of all persons involved in the system were invested in low-risk assets. Over the past five years, the profitability of the aforementioned portfolio amounted to 49% which corresponds to the annual 9.3% rate. Against inflation, this stable (less risky) portfolio showed a total return of 10.13% and an annual average return of 2.17%.

Low-risk assets mainly include bank deposits and bonds as well as a small amount of foreign currency and stocks. In high-risk areas, on the contrary, the share of foreign assets may reach the 60% limit stipulated by the law. A medium-risk package is a mix of the first two.

As clarified by the Pension Agency, investing in shares increases profitability, the nominal benefit exceeds inflation whilst diversification becomes possible.

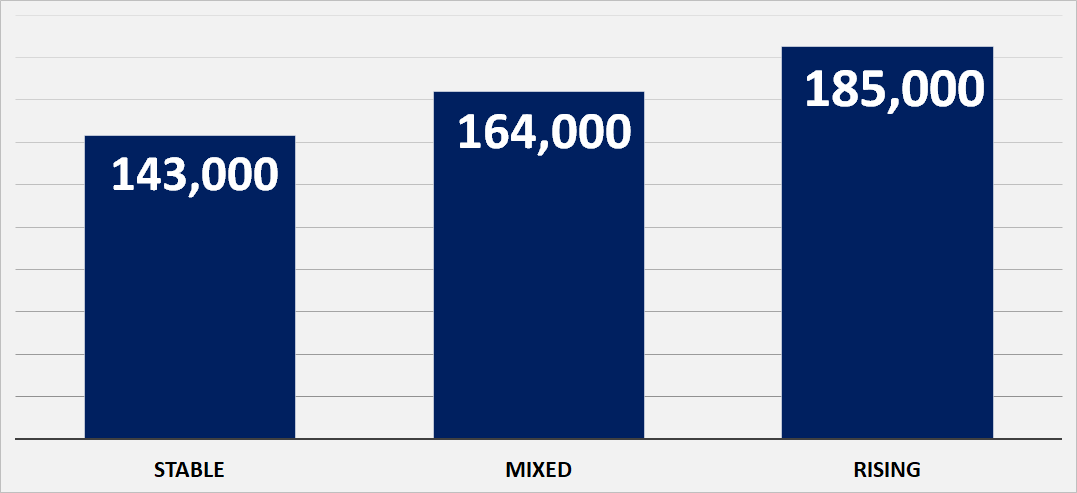

According to the agency's calculations, when making a monthly contribution of GEL 100, the estimated amount of savings should reach GEL 143,000 in a stable portfolio investment after 35 years. In the case of a mixed investment, the savings should be GEL 164,000. In the case of a high-risk investment – GEL 185,000. According to these calculations, which are based on an assumption, investing in high-risk assets increases the amount of savings in the long term by an average of 29% as compared to stable assets.

Graph 1: Estimated Returns on Monthly GEL 100 Contribution for 35 Years (Calculation is Based on Assumption)

Source: Pension Agency

In accordance with the Pension Agency’s decision, 60% of assets in the low-risk portfolio will be invested in bank deposits in GEL whilst the share of bank deposit in local currency will be 25% in the rising portfolio.

Table 1:Asset Distribution Scheme

Source: Pension Agency

Stock investments are generally considered riskier as compared to investment in deposits. However, the investment policy document provides some insurance tools. The Pension Agency is not allowed to purchase just any security. Stocks/bonds purchased by the Pension Agency should meet the criteria as follows:

1.Have a credit rating from at least one global rating agency (Standard & Poor’s, Moody’s, Fitch Ratings, Scope Ratings).

2. Minimum rating for the resident entity or the financial instruments issued by the resident entity is defined as one notch below a sovereign credit rating of Georgia. Weight of such financial instruments in the Investment Portfolio shall not exceed 10% of the Pension Assets.

3. Minimum rating for the non-resident entity or the financial instruments issued by a non-resident entity (including those issued by financial institutions) is defined as BBB-/Baa3 or equivalent.

4. Cash and deposits can only be held in at least A-/A3 or equivalent rated non-resident financial institution or in a licensed domestic commercial bank with a credit rating from at least one global rating agency (Standard & Poor’s, Moody’s, Fitch Ratings, Scope Ratings).

More information about credit ratings and their importance can be found in FactCheck’s previous articles (link 1, link 2).

As of 31 July 2023, the net value of pension assets was GEL 3.76 billion. Of this amount, GEL 680 million is a net return from investments. The number of people involved in the pension plan is 1.4 million. At that time, some 4,811 individuals have already made use of the cumulative pension and have received GEL 12.3 million in pension.