The issue of building new hydroelectric plants and a subsequent increase in electricity tariffs has become pressing recently in Georgia. On 20 September 2018, Rustavi 2 was the first to report this news based on a World Bank report.

The Ministry of Economy and Sustainable Development of Georgia rejects this claim. The Ministry stated: “Information that electricity tariffs will increase drastically as a result of building HPPs is a blatant lie.”

Before we move on to a discussion of a possible increase in electricity tariffs, it would be appropriate to review their structure. The consumer tariff, which is paid by a citizen, can be roughly divided into two components: the price to pay the producer (HPP, TPP, etc.) and the price to pay for transportation from the producer to the consumer (transfer, distribution, transmission, dispatching, etc.). Naturally, an increase in each of these components will result in an increased consumer tariff. In accordance with the aforementioned information, the electricity tariff will be increased because of the increase in the component of the fee which is paid to the producer.

Of note is that the electricity price (selling price) is calculated based on producer expenses and it varies for different producers. For instance,[1] the Inguri HPP’s selling price for electricity is GEL 0.01818 for kwt/h whilst the Vardnili HPP cascade’s selling price is GEL 0.04002. Given the fact that the consumer tariff is the same for all, it is calculated on the basis of the weighted price. For instance, if the Inguri HPP produced 100 kwt/h of energy and the Vardnili HPP cascade produced 10 kwt/h of energy, the total price for 110 kwt/h of energy will be GEL 2.2181; that is, the average price for one kwt/h will be GEL 0.0202. The transportation tariff is then added to this figure which determines the consumer tariff rate. If a third producer appears, which produced an additional 10 kwt/h of energy for a GEL 0.1 tariff for one kwt/h of energy, then the total price for 120 kwt/h of energy will reach GEL 3.2182. The average tariff for one kwt/h will be increased from GEL 0.202 to GEL 0.268. The transportation component being unchanged will still increase the consumer tariff. Therefore, the new producer which sells electricity for a higher than weighted price will increase the average weighted price and provoke a growth in the consumer tariff rate.

Information about the growth in the electricity tariff is based on a World Bank report published on 22 February 2018. The document was prepared by World Bank employees and compiled as a report of the Ministry of Finance of Georgia to study the possible impact of signed power purchase agreements (PPA)[2] or those under discussion upon fiscal expenditures and tariffs. In addition, also at the request of the Ministry of Finance, the report does not take into account the possible impact of the Khudoni HPP construction “because of a lack of clarity associated with the project.” The methodology and approaches employed in the report were agreed with the Ministry of Energy, Ministry of Finance and the Georgian National Energy and Water Supply Regulatory Commission.

In accordance with the report, the Nenskra HPP stipulates the highest fiscal expenditures of all of the projects. Its average annual generation, which is 1.2 billion kwt/h, constitutes 9% of the annual estimated consumption for 2023. In accordance with the purchase agreement, the energy purchase price is USD 0.755 with an annual 3% growth for the next 34 years. This tariff substantially exceeds both the electricity import price[3] as well as the average market price (USD 0.045) on the potential export market (Turkey) at the time the report was written. Therefore, exporting Nenskra HPP produced energy will not balance the expenditure (obligatory purchase price from Nenskra HPP) and the result will be a net loss according to the assessment of the World Bank.

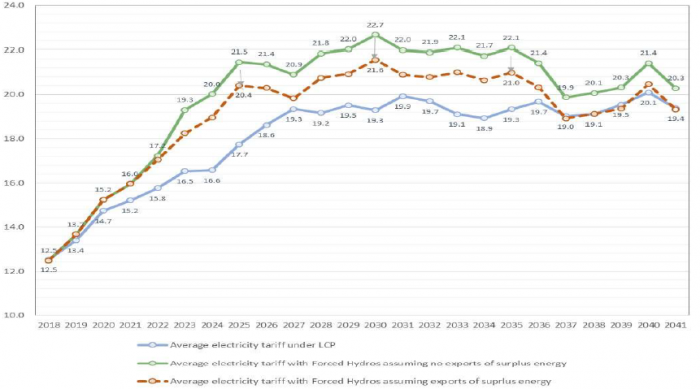

Graph 1 illustrates the possible impact of the construction of new HPPs upon the average electricity price in Georgia. Based on the assessment of the World Bank, it shows that launching new projects will substantially increase average tariffs because of energy purchase agreement conditions.

Graph 1: Average Electricity Tariff (GEL on Kwt/h) in Different Scenarios[4]

Source: World Bank Assessment

The blue line on the graph shows the changes in the wholesale tariff in the case of the so-called optimum scenario; that is, when only those HPPs are built which will be sufficient for meeting the local demand. The electricity tariff is the lowest in this scenario. In the case if all of the planned HPPs are built, including those under discussion, the tariff will increase more as compared to the optimum scenario. However, even in the case of building all of the HPPs, there are two alternative scenarios: the green line shows the extreme and theoretically less feasible case when surplus energy (energy production minus local consumption) cannot be exported. In other words, the state takes an obligation to purchase that surplus energy; however, because of a lack of consumers or an acceptable export price, it is unable to sell it abroad. This energy will be lost given the impossibility of accumulating or storing electricity. The third (red line) scenario is stuck between the two extremes when all of the planned HPPs are built but the surplus energy is exported at 85% of the existing market price. Finally, it can be said that the electricity tariff will increase in any case although this increase will be more as compared to the optimum scenario if all of the new HPPs are built.

At the same time, whilst interpreting the main findings of the document, we have to take into account that the estimated results are based on the expected unfolding of events and the conditions of sound assumptions and these results will only be brought if these conditions are met. If conditions change, the final results will also naturally change. For instance, the export price to Turkey can be changed, memoranda on the construction of HPPs could be amended or local consumption could be increased faster than expected, all of which will create the need for new generating facilities.

The Georgian public has a constant and painful perception of the possible increase in electricity tariffs. However, one also needs to take into account some objective circumstances which will show that an increase in electricity tariffs is not out of context. Specifically, in light of the current economic development, an increase in prices is a common occurrence and prices will increase for electricity and for almost any other products or services in the future. On the other hand, the rise in electricity consumption, characteristic for economic growth, will inevitably bring the necessity for increasing the tariff. This is because it is necessary to use new and relatively more expensive sources of energy in order to meet the increased demand.

It is neither possible nor desirable to keep a tariff at an artificially low level because this decision will engender indirect expenses. Specifically, if changes are not reflected in the growth of the consumer tariff in accordance with the assessment given in the World Bank’s report, the state will have quasi-fiscal expenses. Further specifically, the electricity system commercial operator (ESCO) is obliged to purchase energy at high prices from the new HPPs. If the consumer tariff is kept at an artificially low level, then financial damage will be inflicted to the ESCO. Given the fact that the ESCO is state-owned, this damage represents an indirect state loss.

Whilst speaking about the Nenskra HPP in particular, the International Monetary Fund’s (IMF) assessment also needs to be taken into account. The IMF’s Fiscal Transparency Evaluation mentions the power purchase agreement (PPA) for the Nenskra HPP produced energy as having some “unique characteristics.” Specifically, the document emphasises the government guarantee for a 12.5% rate of return. Furthermore, the government has also guaranteed against construction and hydrology risks with this agreement which is unlike any other cases. In accordance with the IMF’s assessment, all the aforementioned bears additional fiscal risks.

[1] This provides an example of a more simplified understanding of the concept of the tariff calculation methodology. More details can be accessed at the link.

[2] Nenskra HPP, Namakhvani HPP Cascade (Namakhvani and Tvishi), Koromkheti HPP, etc.

[3] For the report preparation time: Azerbaijan – USD 0.038, Russia – USD 0.053-0.063.

[4] Blue Line - LCP (combination of the least costs within the framework of meeting local energy consumption estimates); Red Line – building new HPPs in accordance with the government plan, surplus energy is exported; Green Line – building new HPPs in accordance with the government plan, surplus energy is not exported.

Source: World Bank Assessment

The blue line on the graph shows the changes in the wholesale tariff in the case of the so-called optimum scenario; that is, when only those HPPs are built which will be sufficient for meeting the local demand. The electricity tariff is the lowest in this scenario. In the case if all of the planned HPPs are built, including those under discussion, the tariff will increase more as compared to the optimum scenario. However, even in the case of building all of the HPPs, there are two alternative scenarios: the green line shows the extreme and theoretically less feasible case when surplus energy (energy production minus local consumption) cannot be exported. In other words, the state takes an obligation to purchase that surplus energy; however, because of a lack of consumers or an acceptable export price, it is unable to sell it abroad. This energy will be lost given the impossibility of accumulating or storing electricity. The third (red line) scenario is stuck between the two extremes when all of the planned HPPs are built but the surplus energy is exported at 85% of the existing market price. Finally, it can be said that the electricity tariff will increase in any case although this increase will be more as compared to the optimum scenario if all of the new HPPs are built.

At the same time, whilst interpreting the main findings of the document, we have to take into account that the estimated results are based on the expected unfolding of events and the conditions of sound assumptions and these results will only be brought if these conditions are met. If conditions change, the final results will also naturally change. For instance, the export price to Turkey can be changed, memoranda on the construction of HPPs could be amended or local consumption could be increased faster than expected, all of which will create the need for new generating facilities.

The Georgian public has a constant and painful perception of the possible increase in electricity tariffs. However, one also needs to take into account some objective circumstances which will show that an increase in electricity tariffs is not out of context. Specifically, in light of the current economic development, an increase in prices is a common occurrence and prices will increase for electricity and for almost any other products or services in the future. On the other hand, the rise in electricity consumption, characteristic for economic growth, will inevitably bring the necessity for increasing the tariff. This is because it is necessary to use new and relatively more expensive sources of energy in order to meet the increased demand.

It is neither possible nor desirable to keep a tariff at an artificially low level because this decision will engender indirect expenses. Specifically, if changes are not reflected in the growth of the consumer tariff in accordance with the assessment given in the World Bank’s report, the state will have quasi-fiscal expenses. Further specifically, the electricity system commercial operator (ESCO) is obliged to purchase energy at high prices from the new HPPs. If the consumer tariff is kept at an artificially low level, then financial damage will be inflicted to the ESCO. Given the fact that the ESCO is state-owned, this damage represents an indirect state loss.

Whilst speaking about the Nenskra HPP in particular, the International Monetary Fund’s (IMF) assessment also needs to be taken into account. The IMF’s Fiscal Transparency Evaluation mentions the power purchase agreement (PPA) for the Nenskra HPP produced energy as having some “unique characteristics.” Specifically, the document emphasises the government guarantee for a 12.5% rate of return. Furthermore, the government has also guaranteed against construction and hydrology risks with this agreement which is unlike any other cases. In accordance with the IMF’s assessment, all the aforementioned bears additional fiscal risks.

[1] This provides an example of a more simplified understanding of the concept of the tariff calculation methodology. More details can be accessed at the link.

[2] Nenskra HPP, Namakhvani HPP Cascade (Namakhvani and Tvishi), Koromkheti HPP, etc.

[3] For the report preparation time: Azerbaijan – USD 0.038, Russia – USD 0.053-0.063.

[4] Blue Line - LCP (combination of the least costs within the framework of meeting local energy consumption estimates); Red Line – building new HPPs in accordance with the government plan, surplus energy is exported; Green Line – building new HPPs in accordance with the government plan, surplus energy is not exported.

Source: World Bank Assessment

The blue line on the graph shows the changes in the wholesale tariff in the case of the so-called optimum scenario; that is, when only those HPPs are built which will be sufficient for meeting the local demand. The electricity tariff is the lowest in this scenario. In the case if all of the planned HPPs are built, including those under discussion, the tariff will increase more as compared to the optimum scenario. However, even in the case of building all of the HPPs, there are two alternative scenarios: the green line shows the extreme and theoretically less feasible case when surplus energy (energy production minus local consumption) cannot be exported. In other words, the state takes an obligation to purchase that surplus energy; however, because of a lack of consumers or an acceptable export price, it is unable to sell it abroad. This energy will be lost given the impossibility of accumulating or storing electricity. The third (red line) scenario is stuck between the two extremes when all of the planned HPPs are built but the surplus energy is exported at 85% of the existing market price. Finally, it can be said that the electricity tariff will increase in any case although this increase will be more as compared to the optimum scenario if all of the new HPPs are built.

At the same time, whilst interpreting the main findings of the document, we have to take into account that the estimated results are based on the expected unfolding of events and the conditions of sound assumptions and these results will only be brought if these conditions are met. If conditions change, the final results will also naturally change. For instance, the export price to Turkey can be changed, memoranda on the construction of HPPs could be amended or local consumption could be increased faster than expected, all of which will create the need for new generating facilities.

The Georgian public has a constant and painful perception of the possible increase in electricity tariffs. However, one also needs to take into account some objective circumstances which will show that an increase in electricity tariffs is not out of context. Specifically, in light of the current economic development, an increase in prices is a common occurrence and prices will increase for electricity and for almost any other products or services in the future. On the other hand, the rise in electricity consumption, characteristic for economic growth, will inevitably bring the necessity for increasing the tariff. This is because it is necessary to use new and relatively more expensive sources of energy in order to meet the increased demand.

It is neither possible nor desirable to keep a tariff at an artificially low level because this decision will engender indirect expenses. Specifically, if changes are not reflected in the growth of the consumer tariff in accordance with the assessment given in the World Bank’s report, the state will have quasi-fiscal expenses. Further specifically, the electricity system commercial operator (ESCO) is obliged to purchase energy at high prices from the new HPPs. If the consumer tariff is kept at an artificially low level, then financial damage will be inflicted to the ESCO. Given the fact that the ESCO is state-owned, this damage represents an indirect state loss.

Whilst speaking about the Nenskra HPP in particular, the International Monetary Fund’s (IMF) assessment also needs to be taken into account. The IMF’s Fiscal Transparency Evaluation mentions the power purchase agreement (PPA) for the Nenskra HPP produced energy as having some “unique characteristics.” Specifically, the document emphasises the government guarantee for a 12.5% rate of return. Furthermore, the government has also guaranteed against construction and hydrology risks with this agreement which is unlike any other cases. In accordance with the IMF’s assessment, all the aforementioned bears additional fiscal risks.

[1] This provides an example of a more simplified understanding of the concept of the tariff calculation methodology. More details can be accessed at the link.

[2] Nenskra HPP, Namakhvani HPP Cascade (Namakhvani and Tvishi), Koromkheti HPP, etc.

[3] For the report preparation time: Azerbaijan – USD 0.038, Russia – USD 0.053-0.063.

[4] Blue Line - LCP (combination of the least costs within the framework of meeting local energy consumption estimates); Red Line – building new HPPs in accordance with the government plan, surplus energy is exported; Green Line – building new HPPs in accordance with the government plan, surplus energy is not exported.