Verdict: Sergi Kapanadze’s statement is TRUE.

Resume: The tax burden is the ratio of budget tax incomes to the GDP. It has been increasing since 2013. It increased by 1.9 percentage points in the period of 2013-2017. The tax burden was 24.8% in 2013 with the estimated figure for 2017 having increased to 26.7%.

An increase in the excise tax rate resulted in a 1.3 percentage point growth of the tax burden and 0.6 of a percentage point decrease in the profit tax burden owing to changes in taxation. The Value Added Tax (VAT) burden, after decreasing by one percentage point in 2013, has once again increased.

In short, Georgia’s tax burden has been increasing for the last five years and is currently at its highest level since 2010.

Analysis

At a session of the Parliament of Georgia, European Georgia Movement for Freedom member, Sergi Kapanadze, stated that the Georgian Dream had increased the tax burden. Mr Kapanadze stated that the ratio of tax incomes to the GDP was 24.8% in 2013 and reached 26% in 2017.

There are five types of national taxes in Georgia. This number did not change after the Georgian Dream came to power. However, some of the tax rates and taxation subjects did indeed change.

Excise Tax: Taxable transactions as well as the export and import of excised goods are subjects of excise tax. The excise tax rate is differentiated for certain types of goods. Of the 11 taxable groups of goods, the excise tax rate increased for vehicle imports. In addition, the excise tax rate increased significantly on tobacco products. From 2013, the excise tax rate for a 20-package of filtered cigarettes increased from GEL 0.6 to GEL 1.7 whilst the excise tax rate for a 20-package of unfiltered cigarettes increased from GEL 0.15 to GEL 0.6. The excise tax rate for fuel products has also increased from 2017. It went up from GEL 250 to GEL 500 for one tonne of petroleum and from GEL 150 to GEL 400 for one tonne of diesel. The excise tax rate also increased for natural gas used as vehicle fuel. It increased from GEL 80 per 1,000 cubic metres to GEL 200. The excise tax hike on petroleum products has significantly affected local fuel prices. The increase in the price of diesel has been the highest (36.5%). Information in regard to fuel prices before 2017 can be found in FactCheck’s research. In addition, mobile communications services were also a subject of excise tax until 2018. Initially, the services were taxed at 10%. The rate decreased to 8% in 2016 and to 3% in 2017. Currently, this tax has been abolished for all but international calls.

Income Tax: An individual’s income is subject to an income tax of 20%. There have been no changes to income tax in the last years with the only exception being income received from renting or selling property (its tax rate decreased to 5%). However, in accordance with amendments to the Tax Code of Georgia enacted on 20 December 2012, those articles in the code which envisioned the gradual reduction of the income tax rate were removed from the list of transitional provisions. Specifically, in the period between 1 January 2013 and 1 January 2014, the income tax rate was to be reduced to 18% and then further decreased to 15% from 1 January 2014. The article regarding these changes was removed before it came into force with the idea of decreasing the income tax rate being rejected altogether. The new coalition government believed that a decrease in the income tax rate could not have had any impact upon the low-income segment of the population and instead introduced the so-called “Untaxed Minimum.” This envisioned tax returns for individuals with a yearly income of less than GEL 6,000. However, the aforementioned tax preference was only in force from 2013-2014.

Profit Tax and Value Added Tax (VAT): The rates for both of these taxes have not changed since 2012. The difference between the total incomes and the total expenses of an enterprise is taxable by profit tax at a rate of 15%. However, as a result of changes enacted in May 2016, only distributed income has been taxable starting from 2017. The VAT rate is 18% with imported goods as well as the delivery of goods and services valued at more than GEL 100,000 in one calendar year subjected to the tax.

Import Tax: Import tax is applied to the customs duty on imported goods. The import tax rate constitutes 12% and 5% according to particular groups of goods. There are different import tax rates for vehicles and alcoholic beverages. The import tax rates have not changed under the Georgian Dream government.

Property Tax: Income generated by the collection of property tax is fully channelled to the budget of a self-governing entity which determines its rate and which should not exceed 1% annually. A property’s value is subject to property tax. The property tax rate ceiling has not been altered since 2012.

It is necessary to calculate the consolidated budget tax incomes to the nominal GDP in order to determine the amount of the tax burden. To do this, we have to calculate the percentage of income going to taxes which was generated from goods and services delivered to the country in the period of one year.

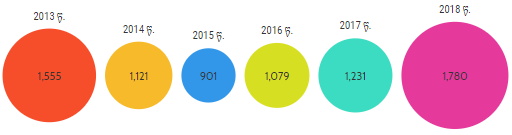

Table 1: Tax Income (%) in 2010-2017

Note* Estimated GDP and tax incomes for a budget year

As we see, the tax burden has had a tendency of growth in the last years and is at 26.7% according to 2017 estimates. Of note is that the Government of Georgia plans to reduce the tax burden to 25% in accordance with its Social and Economic Development Strategy – 2020 although the trend does show the opposite.

Apart from the aforementioned figures, it is important to see the ratio of the taxes to the GDP as well as the tendency of their changes as a result of changes in tax rates and taxable subjects.

Graph 2: Tax Burden in 2010-2017, Given Per Each Type of Tax (%)

Note* Estimated GDP and tax incomes for a budget year

As we see, the tax burden has had a tendency of growth in the last years and is at 26.7% according to 2017 estimates. Of note is that the Government of Georgia plans to reduce the tax burden to 25% in accordance with its Social and Economic Development Strategy – 2020 although the trend does show the opposite.

Apart from the aforementioned figures, it is important to see the ratio of the taxes to the GDP as well as the tendency of their changes as a result of changes in tax rates and taxable subjects.

Graph 2: Tax Burden in 2010-2017, Given Per Each Type of Tax (%)

Note* Estimated GDP and tax incomes for a calendar year

Of the country’s different taxes, the tax burden increased the most (1.3%) in the case of excise tax in 2013-2017. In this same period, the income tax burden increased by 0.8 percentage points whilst the profit tax burden decreased by 0.6 percentage points. As compared to 2013, the VAT burden increased by 0.7 percentage points.

Note* Estimated GDP and tax incomes for a calendar year

Of the country’s different taxes, the tax burden increased the most (1.3%) in the case of excise tax in 2013-2017. In this same period, the income tax burden increased by 0.8 percentage points whilst the profit tax burden decreased by 0.6 percentage points. As compared to 2013, the VAT burden increased by 0.7 percentage points.

Note* Estimated GDP and tax incomes for a budget year

As we see, the tax burden has had a tendency of growth in the last years and is at 26.7% according to 2017 estimates. Of note is that the Government of Georgia plans to reduce the tax burden to 25% in accordance with its Social and Economic Development Strategy – 2020 although the trend does show the opposite.

Apart from the aforementioned figures, it is important to see the ratio of the taxes to the GDP as well as the tendency of their changes as a result of changes in tax rates and taxable subjects.

Graph 2: Tax Burden in 2010-2017, Given Per Each Type of Tax (%)

Note* Estimated GDP and tax incomes for a calendar year

Of the country’s different taxes, the tax burden increased the most (1.3%) in the case of excise tax in 2013-2017. In this same period, the income tax burden increased by 0.8 percentage points whilst the profit tax burden decreased by 0.6 percentage points. As compared to 2013, the VAT burden increased by 0.7 percentage points.

Tags: