On 21 September 2015, the Prime Minister of Georgia held a meeting with members of the Government of Georgia’s Economic Team and the President of the National Bank of Georgia. The main topic of discussion at the meeting was the depreciation of GEL. After the meeting, the Minister of Finance of Georgia, Nodar Khaduri, stated that the macroeconomic factors negatively influencing the GEL exchange rate have been completely eradicated and that the government is expecting a strengthening of GEL.

FactCheck checked whether or not the macroeconomic factors negatively influencing the GEL exchange rate have, in fact, been eradicated.

The main macroeconomic factors influencing the GEL exchange rate are the influx and outflow of foreign currency (which manifests itself in the country’s payment balance), the amount of GEL in the national economy and the economy’s growth rate. The aforementioned factors are influenced by both external factors (the internal economic situation in partner countries) as well as by the monetary (cash and loan policies exercised by the National Bank of Georgia) and fiscal (budgetary and taxation policies determined by the Government of Georgia and exercised by the Ministry of Finance of Georgia) policies of the country.

A major factor contributing to the significant depreciation of GEL in the past ten months has been the decrease in the influx of foreign currency into the country (FactCheck has published several articles about this issue: link 1, link 2, link 3). Foreign currency influx from exports and money transfers has dropped the most of all. Exports started to decrease from August 2014 and have fallen by USD 239 million in the last five months of the year whilst imports have kept increasing. Hence, Georgia’s foreign trade deficit in 2014 increased by USD 253 million as compared to 2013. The current balance deficit (which, apart from the trade of goods also includes trade with services, money transfers and factor incomes) worsened by USD 682 million. Money transfers from abroad started to decrease in October 2014 and dropped by USD 67 million in the last three months of the year. A decrease in exports and money transfers continued in 2015 as well. Exports fell by USD 455 million from January to August 2015 whilst money transfers dropped by USD 250 million. If we summarise the losses of the previous and the current years, the income from exports and money transfers decreased by USD 1 billion. This loss was not compensated by the growth in tourism, credit capital and investments which had a significantly negative influence upon the GEL exchange rate.

As already mentioned above, exports and money transfers are continuing to drop; however, from January 2015, imports started to fall as well with imports having decreased by USD 562 million from January to August 2015. The drop in imports exceeded that of exports and as a result the country’s trade balance from January to August 2015 improved by USD 107 million as compared to the same period of the previous year. The decrease in imports was due to imported products becoming more expensive. This is one of the macroeconomic factors whose negative influence has been eradicated. However, including the decrease in money transfers, USD 143 million less income was generated from external trade and money transfers from January to August 2015 as compared to the same period of 2014.

In order to decisively say that more foreign currency is entering the country than is leaving, it is necessary to have the data of the last several months as concerns other sources of foreign currency (investments, tourism, loans and so on). This information will be completely described in the payment balance of the third quarter of 2015 which will be published in December 2015. As of yet, we only know the payment balance of the first two quarters of 2015 according to which USD 165 million less in foreign currency entered Georgia rather than left the country. It is also known that the negative trade balance from January to August 2015 amounted to USD 3.5 billion. It unknown to what extent this deficit was covered by other sources of USD.

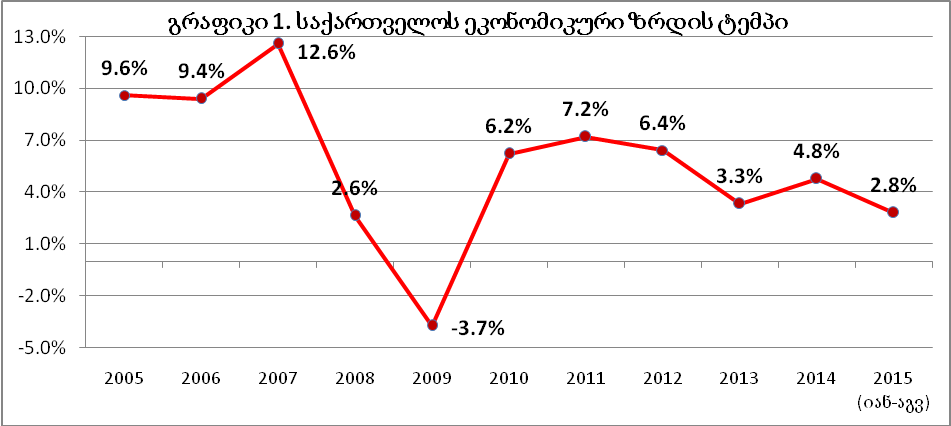

The harm to the GEL exchange rate caused by the drop in the influx of foreign currency can be significantly relieved by monetary policy. This requires a so-called strict monetary policy which will ultimately result in the decrease in the amount of GEL in the economy or at least keeping it at a certain fixed level. The amount of reserve money (excluding foreign currency) which includes the amount of GEL issued by the National Bank of Georgia increased by 7% (GEL 191 million) during the past year (Chart 1).

Chart 1: Changes in the Amount of GEL in the Economy in 2015 as Compared to the Same Period of the Previous Year

Naturally, the decrease in the growth rate of the amount of GEL in the economy or keeping it at a steady level is achievable; however, the current growth rate corresponds to the growth rate of the Georgian economy. If the National Bank tightened its monetary policy to the point that the amount of GEL in circulation would not grow, it would achieve the goal of a temporary stability of the exchange rate; however, this would also put the economy into recession. In addition, in the case of an artificially maintained low exchange rate, Georgia’s external trade balance would further worsen (due to the drop in exports at a higher level than that of import) and the GEL exchange rate would depreciate all the same in the future.

The National Bank of Georgia started tightening its monetary policy (increasing the interest rate of the refinancing loan) from February 2015 and put it up from 4% to 7%. The latest increase in the interest rate was recorded on 23 September 2015 and its influence upon the exchange rate will manifest itself gradually. In other similar conditions, the tightening of the monetary policy in this manner would be followed by a decrease in the amount of money in circulation. The main reason for tightening monetary policy is inflation. The annual rate of inflation passed the 5% marker at the end of August 2015.

The government’s fiscal policy; namely, budget expenses, has also influenced the GEL exchange rate during the past few years. FactCheck wrote about this issue earlier as well. Georgia has a deficit state budget which means that the budget spends more money than it receives through its income part. If we look at the spending by months, the state budget had a high level of deficit in February, April, June and August 2015. In these months the deficit was financed using the cash balance which directly caused the growth in the amount of GEL in the economy. In addition, an expansive spending policy encourages imports. The Government of Georgia failed to decrease the spending part of the state budget in July 2015 even though it was planning to lower expenditure by GEL 250 million in spring 2015. It should be noted that according to the amendments to the state budget, the amount of planned domestic loans was decreased by GEL 100 million which will have a positive influence upon the GEL exchange rate. Avoiding a high level of deficit spending from the state budget in the last months of 2015 would be needed in order to eradicate state budget pressure upon GEL. This definitely did not happen in 2013 and 2014.

As of today, the main argument for the stability of GEL is that it has already shown a significant depreciation. When a country has a floating exchange rate, this in itself becomes the means for overcoming the crisis. The depreciation of GEL has already caused a drop in imports which in its turn compensates for the decrease in the influx of USD into the country. Hence, it is true that the macroeconomic factors negatively influencing the GEL exchange rate have been eradicated as they have already manifested themselves in the depreciated exchange rate; however, the exchange rate will maintain its stability if these factors do not worsen in the future. It would be hard to say that they will not worsen as we have already seen numerous precedents. Since the end of February 2015, Cabinet members have been quoted as saying that the factors negatively influencing GEL have been stopped and that they are expecting a stabilisation. In fact, the GEL exchange rate relies upon the market and the tightened monetary policy alone as the budget deficit has not decreased, foreign direct investments have only slightly increased and revenues from privatisation have reached USD 50 million instead of the promised USD 300 million. In addition, sharp macroeconomic measures for encouraging businesses (lowering taxes and decreasing regulations) have not yet taken place.

Conclusion

The main reason for the depreciation of GEL is the decrease in the influx of USD into the country. Imports started to drop from April 2015 which means that less foreign currency is leaving the country and this has significantly balanced the shortfall in the amount of foreign currency. Apart from trade, important sources of USD include tourism, money transfers, investments and loans. Money transfers are still on the decrease whilst the information about the remaining factors will be published in three months. Hence, it is difficult to say whether or not the external factors negatively influencing the exchange rate have completely exhausted themselves. Only the trends of import can be a cause for hope.

The increase in the amount of GEL in circulation has not been the reason for the depreciation of GEL; however, by manipulating this amount, the National Bank can facilitate the stability of the exchange rate. The amount of GEL in the economy has increased by approximately 7% and the National Bank has once again tightened its monetary policy. This will facilitate the stability of the exchange rate.

Georgia’s fiscal policy is mainly focused upon social affairs which has manifested itself in a low facilitation of economic growth as well as in the increased budget deficit and the state’s external debt. The budget has a periodic negative influence upon the GEL exchange rate. In the last months of 2015 it will become necessary for the government not to use the deposit money and decrease its spending as necessary.

To summarise, the general image is as follows: the macroeconomic problems up to this point have caused the national currency to depreciate by 37%. The current GEL exchange rate will be maintained if these factors are not further worsened in the future. As the domestic problems in the economies of Georgia’s top trade partner countries are still on-going and the stability of GEL relies upon the anti-crisis effect of the floating exchange rate and the country’s monetary policy, it is hard to predict what will happen to GEL in the future.

FactCheck leaves Nodar Khaduri’s statement WITHOUT VERDICT.

Naturally, the decrease in the growth rate of the amount of GEL in the economy or keeping it at a steady level is achievable; however, the current growth rate corresponds to the growth rate of the Georgian economy. If the National Bank tightened its monetary policy to the point that the amount of GEL in circulation would not grow, it would achieve the goal of a temporary stability of the exchange rate; however, this would also put the economy into recession. In addition, in the case of an artificially maintained low exchange rate, Georgia’s external trade balance would further worsen (due to the drop in exports at a higher level than that of import) and the GEL exchange rate would depreciate all the same in the future.

The National Bank of Georgia started tightening its monetary policy (increasing the interest rate of the refinancing loan) from February 2015 and put it up from 4% to 7%. The latest increase in the interest rate was recorded on 23 September 2015 and its influence upon the exchange rate will manifest itself gradually. In other similar conditions, the tightening of the monetary policy in this manner would be followed by a decrease in the amount of money in circulation. The main reason for tightening monetary policy is inflation. The annual rate of inflation passed the 5% marker at the end of August 2015.

The government’s fiscal policy; namely, budget expenses, has also influenced the GEL exchange rate during the past few years. FactCheck wrote about this issue earlier as well. Georgia has a deficit state budget which means that the budget spends more money than it receives through its income part. If we look at the spending by months, the state budget had a high level of deficit in February, April, June and August 2015. In these months the deficit was financed using the cash balance which directly caused the growth in the amount of GEL in the economy. In addition, an expansive spending policy encourages imports. The Government of Georgia failed to decrease the spending part of the state budget in July 2015 even though it was planning to lower expenditure by GEL 250 million in spring 2015. It should be noted that according to the amendments to the state budget, the amount of planned domestic loans was decreased by GEL 100 million which will have a positive influence upon the GEL exchange rate. Avoiding a high level of deficit spending from the state budget in the last months of 2015 would be needed in order to eradicate state budget pressure upon GEL. This definitely did not happen in 2013 and 2014.

As of today, the main argument for the stability of GEL is that it has already shown a significant depreciation. When a country has a floating exchange rate, this in itself becomes the means for overcoming the crisis. The depreciation of GEL has already caused a drop in imports which in its turn compensates for the decrease in the influx of USD into the country. Hence, it is true that the macroeconomic factors negatively influencing the GEL exchange rate have been eradicated as they have already manifested themselves in the depreciated exchange rate; however, the exchange rate will maintain its stability if these factors do not worsen in the future. It would be hard to say that they will not worsen as we have already seen numerous precedents. Since the end of February 2015, Cabinet members have been quoted as saying that the factors negatively influencing GEL have been stopped and that they are expecting a stabilisation. In fact, the GEL exchange rate relies upon the market and the tightened monetary policy alone as the budget deficit has not decreased, foreign direct investments have only slightly increased and revenues from privatisation have reached USD 50 million instead of the promised USD 300 million. In addition, sharp macroeconomic measures for encouraging businesses (lowering taxes and decreasing regulations) have not yet taken place.

Conclusion

The main reason for the depreciation of GEL is the decrease in the influx of USD into the country. Imports started to drop from April 2015 which means that less foreign currency is leaving the country and this has significantly balanced the shortfall in the amount of foreign currency. Apart from trade, important sources of USD include tourism, money transfers, investments and loans. Money transfers are still on the decrease whilst the information about the remaining factors will be published in three months. Hence, it is difficult to say whether or not the external factors negatively influencing the exchange rate have completely exhausted themselves. Only the trends of import can be a cause for hope.

The increase in the amount of GEL in circulation has not been the reason for the depreciation of GEL; however, by manipulating this amount, the National Bank can facilitate the stability of the exchange rate. The amount of GEL in the economy has increased by approximately 7% and the National Bank has once again tightened its monetary policy. This will facilitate the stability of the exchange rate.

Georgia’s fiscal policy is mainly focused upon social affairs which has manifested itself in a low facilitation of economic growth as well as in the increased budget deficit and the state’s external debt. The budget has a periodic negative influence upon the GEL exchange rate. In the last months of 2015 it will become necessary for the government not to use the deposit money and decrease its spending as necessary.

To summarise, the general image is as follows: the macroeconomic problems up to this point have caused the national currency to depreciate by 37%. The current GEL exchange rate will be maintained if these factors are not further worsened in the future. As the domestic problems in the economies of Georgia’s top trade partner countries are still on-going and the stability of GEL relies upon the anti-crisis effect of the floating exchange rate and the country’s monetary policy, it is hard to predict what will happen to GEL in the future.

FactCheck leaves Nodar Khaduri’s statement WITHOUT VERDICT.

Naturally, the decrease in the growth rate of the amount of GEL in the economy or keeping it at a steady level is achievable; however, the current growth rate corresponds to the growth rate of the Georgian economy. If the National Bank tightened its monetary policy to the point that the amount of GEL in circulation would not grow, it would achieve the goal of a temporary stability of the exchange rate; however, this would also put the economy into recession. In addition, in the case of an artificially maintained low exchange rate, Georgia’s external trade balance would further worsen (due to the drop in exports at a higher level than that of import) and the GEL exchange rate would depreciate all the same in the future.

The National Bank of Georgia started tightening its monetary policy (increasing the interest rate of the refinancing loan) from February 2015 and put it up from 4% to 7%. The latest increase in the interest rate was recorded on 23 September 2015 and its influence upon the exchange rate will manifest itself gradually. In other similar conditions, the tightening of the monetary policy in this manner would be followed by a decrease in the amount of money in circulation. The main reason for tightening monetary policy is inflation. The annual rate of inflation passed the 5% marker at the end of August 2015.

The government’s fiscal policy; namely, budget expenses, has also influenced the GEL exchange rate during the past few years. FactCheck wrote about this issue earlier as well. Georgia has a deficit state budget which means that the budget spends more money than it receives through its income part. If we look at the spending by months, the state budget had a high level of deficit in February, April, June and August 2015. In these months the deficit was financed using the cash balance which directly caused the growth in the amount of GEL in the economy. In addition, an expansive spending policy encourages imports. The Government of Georgia failed to decrease the spending part of the state budget in July 2015 even though it was planning to lower expenditure by GEL 250 million in spring 2015. It should be noted that according to the amendments to the state budget, the amount of planned domestic loans was decreased by GEL 100 million which will have a positive influence upon the GEL exchange rate. Avoiding a high level of deficit spending from the state budget in the last months of 2015 would be needed in order to eradicate state budget pressure upon GEL. This definitely did not happen in 2013 and 2014.

As of today, the main argument for the stability of GEL is that it has already shown a significant depreciation. When a country has a floating exchange rate, this in itself becomes the means for overcoming the crisis. The depreciation of GEL has already caused a drop in imports which in its turn compensates for the decrease in the influx of USD into the country. Hence, it is true that the macroeconomic factors negatively influencing the GEL exchange rate have been eradicated as they have already manifested themselves in the depreciated exchange rate; however, the exchange rate will maintain its stability if these factors do not worsen in the future. It would be hard to say that they will not worsen as we have already seen numerous precedents. Since the end of February 2015, Cabinet members have been quoted as saying that the factors negatively influencing GEL have been stopped and that they are expecting a stabilisation. In fact, the GEL exchange rate relies upon the market and the tightened monetary policy alone as the budget deficit has not decreased, foreign direct investments have only slightly increased and revenues from privatisation have reached USD 50 million instead of the promised USD 300 million. In addition, sharp macroeconomic measures for encouraging businesses (lowering taxes and decreasing regulations) have not yet taken place.

Conclusion

The main reason for the depreciation of GEL is the decrease in the influx of USD into the country. Imports started to drop from April 2015 which means that less foreign currency is leaving the country and this has significantly balanced the shortfall in the amount of foreign currency. Apart from trade, important sources of USD include tourism, money transfers, investments and loans. Money transfers are still on the decrease whilst the information about the remaining factors will be published in three months. Hence, it is difficult to say whether or not the external factors negatively influencing the exchange rate have completely exhausted themselves. Only the trends of import can be a cause for hope.

The increase in the amount of GEL in circulation has not been the reason for the depreciation of GEL; however, by manipulating this amount, the National Bank can facilitate the stability of the exchange rate. The amount of GEL in the economy has increased by approximately 7% and the National Bank has once again tightened its monetary policy. This will facilitate the stability of the exchange rate.

Georgia’s fiscal policy is mainly focused upon social affairs which has manifested itself in a low facilitation of economic growth as well as in the increased budget deficit and the state’s external debt. The budget has a periodic negative influence upon the GEL exchange rate. In the last months of 2015 it will become necessary for the government not to use the deposit money and decrease its spending as necessary.

To summarise, the general image is as follows: the macroeconomic problems up to this point have caused the national currency to depreciate by 37%. The current GEL exchange rate will be maintained if these factors are not further worsened in the future. As the domestic problems in the economies of Georgia’s top trade partner countries are still on-going and the stability of GEL relies upon the anti-crisis effect of the floating exchange rate and the country’s monetary policy, it is hard to predict what will happen to GEL in the future.

FactCheck leaves Nodar Khaduri’s statement WITHOUT VERDICT.

Tags: