According to the statement of a member of Society 20/30, Mikheil Dundua, "… the debt of commercial banks (as of 31 July 2015) to the National Bank of Georgia amounts to at least GEL 680 million… this indicator was down to just GEL 80 million in the same period of the previous year whilst in 2013 the National Bank of Georgia was the one which owed money to commercial banks. If we look at the correlation between the debt of the commercial banks and the exchange rate of GEL, it constitutes up to 90%... this is the main factor which is responsible for the current GEL exchange rate."

FactCheck verified the accuracy of the aforementioned statement at the request of our reader.

The National Bank of Georgia has been criticised on numerous occasions for increasing the credit resource allocated to commercial banks which, according to some experts, is the main factor for the depreciation of GEL. In debt, Mr Dundua probably means the net debt (commercial bank loans from the National Bank of Georgia minus the deposit certificates owned by the commercial banks themselves). The data mentioned in the statement correspond with the official existing data at the moment of the statement. As of 29 July 2014, the net debt of commercial banks equalled GEL 690 million. The official statistics of 2014 and 2013 also correspond to those mentioned in the statement. However, the interesting fact here is not the correlation between the stated and the actual numbers but the analysis of the approach. Standard mistakes are often made in such issues; namely, when analysing the influence of certain factors upon the GEL exchange rate, the trend is to underscore one of the factors as the most important.

This approach can be seen in the assessment published by Mr Dundua on 24 September 2015 where, when talking about the reasons for the depreciation of GEL, focus is upon the interest rate of the refinancing loans whilst other factors are discarded. The interest rate of the refinancing loan (by the influence upon the amount of money in circulation) is only one of the factors and other factors, such as the influx and the outflow of USD, the amount of GEL in circulation, the demand on GEL and USD and the expectations of the players on the market, are also responsible for the formulation of the exchange rate. These general indicators break down to certain variables during complex analysis: exports and imports, revenues from tourism and foreign investments, money transfers from abroad and the amount of GEL in the economy and so on. The changes in all of these factors formulate the exchange rate of the national currency.

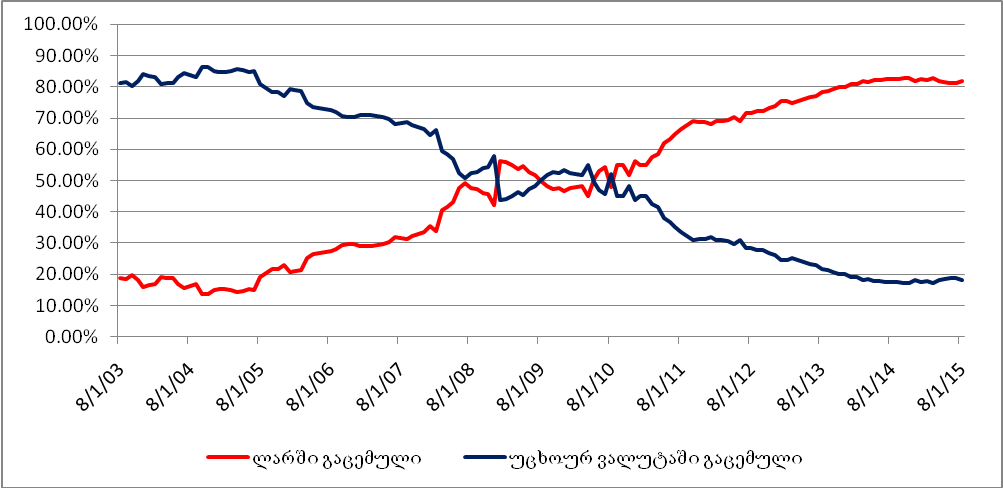

Whilst analysing the influences on the GEL exchange rate, the increase in GEL denominated commercial bank loans given by the National Bank of Georgia should be analysed by its influence upon the changes in the amount of GEL in circulation. Given the fact that the changes in the amount of GEL in the economy tend to be seasonal, it would be more appropriate if we consider the existing data in comparison to the data from the same period of the previous year. An analysis of the money aggregates shows that the M2 aggregate has increased by 7.3% as compared to the same period of the previous year whilst the share of GEL in the reserve money increased by 8.8% and the amount of GEL in the economy increased by 8.3%. Chart 1 depicts the dynamics of the changes in these indicators.

Chart 1: Changes in Money Aggregate as Compared to the Same Period of 2014

Source: National Bank of Georgia

The increase in these aggregates has not played a positive role in the strengthening of the GEL exchange rate; however, claiming that the depreciation was due to this factor only would be quite incorrect just as it is incorrect to try to explain the increase in the amount of reserve money and the amount of GEL in circulation by the growth of the refinancing loans alone. The growth of the amount of money is essential in the case of a positive economic growth rate as the economy will otherwise not be able to grow.

In addition, it must be pointed out that according to the Organic Law of Georgia on the National Bank, unlike the exchange rate stability facilitation, encouraging the sustainable growth of the economy as well as inflation level control – unlike the exchange rate stability facilitation – is definitely one of the main functions of the National Bank of Georgia. Limiting the amount of credit resources in the case of a high demand automatically causes liquidity problems for commercial banks and more expensive credit resources for the national economy, especially given the withdrawal effect caused by balancing the deficit budget using domestic debt. Credit resources becoming much more expensive would automatically cause a slowing down of economic activities and have a negative effect upon both the growth of the nominal GDP as well as the tax revenues of the already deficit budget. Hence, by decreasing the supply of credit resources to commercial banks, a short-term goal of temporarily stabilising the exchange rate of the national currency would be achieved at the expense of causing medium and long-term fundamental economic problems. Despite this, the National Bank of Georgia increased the interest rate of the refinancing loan from 4% to 7% which is due to the expected rate of inflation.

As a matter of fact, the depreciation of GEL is caused by complex reasons. The most important of these is the decrease in the influx of USD into the country which was mainly manifested in the drop in exports and money transfers from abroad. FactCheck wrote about this issue earlier as well.

As for the correlation rate mentioned in the statement and the attempt of using econometric models, first of all it should be pointed out that a high rate of correlation is not a sufficient base to prove causal relations between the factors. Furthermore, any steadily growing correlation rate in the given moment would be high enough, regardless of its connection with the depreciation of GEL. In addition, defining the opening variable – the currency exchange rate – by a single explanatory variable; namely, the debt of commercial banks, leads us to a poorly specified model and a whole set of omitted variables which, in their turn, lead to a positive or negative bias of the explanatory variable coefficient. It should be noted that the omitted variables are a much bigger problem in econometrics than, for example, unnecessarily included ones. Using a single explanatory variable in the model is unjustified and causes mistakes. Especially in the given case we have a time series which is much more complicated to analyse econometrically than regressively and includes issues such as seasonality and the existence of trends. Hence, using the initial form of a time series in a regression leads to a flawed model. These data need to be processed before being analysed. Further, in publishing results, it is necessary to point out the methods which were used for solving the problem and why the specific method was chosen from among all of the alternatives. Making an analysis based upon a separate regressive equation, without any additional information, is inappropriate.

Conclusion

Despite the fact that the commercial bank debt to the National Bank of Georgia had increased by the summer of 2015 as compared to the same period of the previous year, it is still incorrect to state this as a reason for the depreciation of GEL. The legally defined function of the National Bank is to manage inflation and encourage the sustainable development of the economy, not to facilitate the stability of the exchange rate of the national currency. The exchange rate itself is formed as a result of the simultaneous changes of numerous indicators. In the given period of time, the aspects of the majority of these indicators having influence upon the GEL exchange rate were mainly negative (especially external factors). The National Bank of Georgia tightened its monetary policy due to the increased inflation (increasing the refinancing interest rate from 4% to 7%) which will have a positive influence upon the GEL exchange rate.

Using the correlation rate only for proving the causal connection in econometric analysis is unjustified as a high rate of correlation is not a sufficient base to prove causal relations between the factors. Defining the opening variable in a regressive analysis by one explanatory variable only, when the actual number of these variables is much higher, leads to an incorrect result. Using the initial form of a time series in a regression leads to a flawed model and incorrect conclusions.

FactCheck concludes that Mikheil Dundua’s statement is FALSE.

Source: National Bank of Georgia

The increase in these aggregates has not played a positive role in the strengthening of the GEL exchange rate; however, claiming that the depreciation was due to this factor only would be quite incorrect just as it is incorrect to try to explain the increase in the amount of reserve money and the amount of GEL in circulation by the growth of the refinancing loans alone. The growth of the amount of money is essential in the case of a positive economic growth rate as the economy will otherwise not be able to grow.

In addition, it must be pointed out that according to the Organic Law of Georgia on the National Bank, unlike the exchange rate stability facilitation, encouraging the sustainable growth of the economy as well as inflation level control – unlike the exchange rate stability facilitation – is definitely one of the main functions of the National Bank of Georgia. Limiting the amount of credit resources in the case of a high demand automatically causes liquidity problems for commercial banks and more expensive credit resources for the national economy, especially given the withdrawal effect caused by balancing the deficit budget using domestic debt. Credit resources becoming much more expensive would automatically cause a slowing down of economic activities and have a negative effect upon both the growth of the nominal GDP as well as the tax revenues of the already deficit budget. Hence, by decreasing the supply of credit resources to commercial banks, a short-term goal of temporarily stabilising the exchange rate of the national currency would be achieved at the expense of causing medium and long-term fundamental economic problems. Despite this, the National Bank of Georgia increased the interest rate of the refinancing loan from 4% to 7% which is due to the expected rate of inflation.

As a matter of fact, the depreciation of GEL is caused by complex reasons. The most important of these is the decrease in the influx of USD into the country which was mainly manifested in the drop in exports and money transfers from abroad. FactCheck wrote about this issue earlier as well.

As for the correlation rate mentioned in the statement and the attempt of using econometric models, first of all it should be pointed out that a high rate of correlation is not a sufficient base to prove causal relations between the factors. Furthermore, any steadily growing correlation rate in the given moment would be high enough, regardless of its connection with the depreciation of GEL. In addition, defining the opening variable – the currency exchange rate – by a single explanatory variable; namely, the debt of commercial banks, leads us to a poorly specified model and a whole set of omitted variables which, in their turn, lead to a positive or negative bias of the explanatory variable coefficient. It should be noted that the omitted variables are a much bigger problem in econometrics than, for example, unnecessarily included ones. Using a single explanatory variable in the model is unjustified and causes mistakes. Especially in the given case we have a time series which is much more complicated to analyse econometrically than regressively and includes issues such as seasonality and the existence of trends. Hence, using the initial form of a time series in a regression leads to a flawed model. These data need to be processed before being analysed. Further, in publishing results, it is necessary to point out the methods which were used for solving the problem and why the specific method was chosen from among all of the alternatives. Making an analysis based upon a separate regressive equation, without any additional information, is inappropriate.

Conclusion

Despite the fact that the commercial bank debt to the National Bank of Georgia had increased by the summer of 2015 as compared to the same period of the previous year, it is still incorrect to state this as a reason for the depreciation of GEL. The legally defined function of the National Bank is to manage inflation and encourage the sustainable development of the economy, not to facilitate the stability of the exchange rate of the national currency. The exchange rate itself is formed as a result of the simultaneous changes of numerous indicators. In the given period of time, the aspects of the majority of these indicators having influence upon the GEL exchange rate were mainly negative (especially external factors). The National Bank of Georgia tightened its monetary policy due to the increased inflation (increasing the refinancing interest rate from 4% to 7%) which will have a positive influence upon the GEL exchange rate.

Using the correlation rate only for proving the causal connection in econometric analysis is unjustified as a high rate of correlation is not a sufficient base to prove causal relations between the factors. Defining the opening variable in a regressive analysis by one explanatory variable only, when the actual number of these variables is much higher, leads to an incorrect result. Using the initial form of a time series in a regression leads to a flawed model and incorrect conclusions.

FactCheck concludes that Mikheil Dundua’s statement is FALSE.

Source: National Bank of Georgia

The increase in these aggregates has not played a positive role in the strengthening of the GEL exchange rate; however, claiming that the depreciation was due to this factor only would be quite incorrect just as it is incorrect to try to explain the increase in the amount of reserve money and the amount of GEL in circulation by the growth of the refinancing loans alone. The growth of the amount of money is essential in the case of a positive economic growth rate as the economy will otherwise not be able to grow.

In addition, it must be pointed out that according to the Organic Law of Georgia on the National Bank, unlike the exchange rate stability facilitation, encouraging the sustainable growth of the economy as well as inflation level control – unlike the exchange rate stability facilitation – is definitely one of the main functions of the National Bank of Georgia. Limiting the amount of credit resources in the case of a high demand automatically causes liquidity problems for commercial banks and more expensive credit resources for the national economy, especially given the withdrawal effect caused by balancing the deficit budget using domestic debt. Credit resources becoming much more expensive would automatically cause a slowing down of economic activities and have a negative effect upon both the growth of the nominal GDP as well as the tax revenues of the already deficit budget. Hence, by decreasing the supply of credit resources to commercial banks, a short-term goal of temporarily stabilising the exchange rate of the national currency would be achieved at the expense of causing medium and long-term fundamental economic problems. Despite this, the National Bank of Georgia increased the interest rate of the refinancing loan from 4% to 7% which is due to the expected rate of inflation.

As a matter of fact, the depreciation of GEL is caused by complex reasons. The most important of these is the decrease in the influx of USD into the country which was mainly manifested in the drop in exports and money transfers from abroad. FactCheck wrote about this issue earlier as well.

As for the correlation rate mentioned in the statement and the attempt of using econometric models, first of all it should be pointed out that a high rate of correlation is not a sufficient base to prove causal relations between the factors. Furthermore, any steadily growing correlation rate in the given moment would be high enough, regardless of its connection with the depreciation of GEL. In addition, defining the opening variable – the currency exchange rate – by a single explanatory variable; namely, the debt of commercial banks, leads us to a poorly specified model and a whole set of omitted variables which, in their turn, lead to a positive or negative bias of the explanatory variable coefficient. It should be noted that the omitted variables are a much bigger problem in econometrics than, for example, unnecessarily included ones. Using a single explanatory variable in the model is unjustified and causes mistakes. Especially in the given case we have a time series which is much more complicated to analyse econometrically than regressively and includes issues such as seasonality and the existence of trends. Hence, using the initial form of a time series in a regression leads to a flawed model. These data need to be processed before being analysed. Further, in publishing results, it is necessary to point out the methods which were used for solving the problem and why the specific method was chosen from among all of the alternatives. Making an analysis based upon a separate regressive equation, without any additional information, is inappropriate.

Conclusion

Despite the fact that the commercial bank debt to the National Bank of Georgia had increased by the summer of 2015 as compared to the same period of the previous year, it is still incorrect to state this as a reason for the depreciation of GEL. The legally defined function of the National Bank is to manage inflation and encourage the sustainable development of the economy, not to facilitate the stability of the exchange rate of the national currency. The exchange rate itself is formed as a result of the simultaneous changes of numerous indicators. In the given period of time, the aspects of the majority of these indicators having influence upon the GEL exchange rate were mainly negative (especially external factors). The National Bank of Georgia tightened its monetary policy due to the increased inflation (increasing the refinancing interest rate from 4% to 7%) which will have a positive influence upon the GEL exchange rate.

Using the correlation rate only for proving the causal connection in econometric analysis is unjustified as a high rate of correlation is not a sufficient base to prove causal relations between the factors. Defining the opening variable in a regressive analysis by one explanatory variable only, when the actual number of these variables is much higher, leads to an incorrect result. Using the initial form of a time series in a regression leads to a flawed model and incorrect conclusions.

FactCheck concludes that Mikheil Dundua’s statement is FALSE.

Tags: