At the plenary session of the Parliament held on 5 February 2014, Chair of the Committee on Budget and Finance, Davit Onoprishvili, stated: “The exchange rate has practically stabilised now, hovering between 1.77-1.78. The inflation rate is within the established margins. As specified in the State Budget of Georgia, it is not to exceed 6% within a year. I would also like to note that the GEL is not the only currency experiencing a certain decline. Over the course of the last months, the GEL fell by up to 6%. Meanwhile in neighbouring Turkey, the Turkish lira is falling by around 25% and the rate of decline is fairly high in Russia as well; namely, over 10%. These are the major importers in Georgia and, therefore, the strengthening of our currency at this stage would have more detrimental repercussions. The trade parameters took a marked upturn: the growth of [Georgian] export is unprecedentedly high which means that significant changes are underway in this respect, trade balance has decreased and it is positive.”

FactCheck inquired about the accuracy of Davit Onoprishvili’s statement.

As can be gathered from the data of 5 February 2014, the USD/GEL exchange rate equalled 1.7810 whereas as of 9 April it stands at 1.7495 (the GEL has already stabilised and started strengthening). In line with the data of 2013, the inflation rate (CPI) amounted to 2.4% (comparing December of 2013 with the same period of 2012). In January of 2014, as compared to the same month of the preceding year, the inflation rate equalled 2.9% whereas in February of 2014 the indicator reached 3.5%. The monetary policy of the National Bank of Georgia foresees the announcement of an inflation target that should be maintained in the medium term. For the year 2014, the regime of inflation targeting envisages the rate of inflation at 6%, and at 5% for 2015. In the long run, the inflation target should gradually decrease to 3%.

Table 1. USD/GEL, USD/TRY and USD/RUB Exchange Rates

Source: National Bank of Georgia – nbg.ge; x-rates.com

As can be seen in Table 1, over the course of the last five months (as compared to the same period of the past year) the GEL was depreciating with respect to the USD. In October of 2013, the value of the GEL fell by 0.32%, in November – by 0.96%, in December – by 3.19% and in January – by 6.05% (as compared to the same months of the previous year). Calculation of the average indicator for the given period reveals that on the whole, over the months of October, November, December and January, the GEL depreciated by 2.63%. This figure does not correspond to the number indicated in the statement of Davit Onoprishvili (claiming a 6% depreciation of the GEL over the course of the last months). However, if we take into account the indicator for January, separately, we observe that the GEL depreciated by 6.05% relative to January of 2013 and, therefore, the statement of the Chair of the Committee on Budget and Finance proves to be accurate.

As for the exchange rate of the TRY (Turkish lira) against the USD, throughout the last months it has invariably been depreciating in value. In October of 2013, the TRY fell by 10.05% as compared to the same period of 2012, in November – by 12.91%, in December – by 15.65% and in January – by 25.47%. Calculating the average indicator for the fourth quarter of 2013 and January of 2014, we see that the TRY depreciated by 16.02% in the given period. Accordingly, Davit Onoprishvili’s statement regarding a 25% depreciation of the TRY over the span of the last months is inaccurate. Similar to the previous case discussed above, however, in the event of taking into consideration only the month of January, the MP’s statement proves to be correct.

In parallel to the currency depreciations in Turkey and Georgia, the value of the RUB (Russian rouble) saw a decline as well. Specifically, in October 2013 depreciation amounted to 3.02%, in November – 4.20%, in December – 6.97% and in January – 11.61%. Calculating the average indicator for the fourth quarter of 2013 and the month of January of 2014, we get the result of 6.45%. Hence, Davit Onoprishvili’s statement with regard to a 10% depreciation in the value of the RUB is incorrect. Nonetheless, examining the indicator for the month of January, separately, we again come to the conclusion that the MP’s estimations are accurate.

Let us examine Georgia’s import indices in respect to the neighbouring countries.

Table 2. Georgia’s Import Indices (from Russia and Turkey)

Source: National Bank of Georgia – nbg.ge; x-rates.com

As can be seen in Table 1, over the course of the last five months (as compared to the same period of the past year) the GEL was depreciating with respect to the USD. In October of 2013, the value of the GEL fell by 0.32%, in November – by 0.96%, in December – by 3.19% and in January – by 6.05% (as compared to the same months of the previous year). Calculation of the average indicator for the given period reveals that on the whole, over the months of October, November, December and January, the GEL depreciated by 2.63%. This figure does not correspond to the number indicated in the statement of Davit Onoprishvili (claiming a 6% depreciation of the GEL over the course of the last months). However, if we take into account the indicator for January, separately, we observe that the GEL depreciated by 6.05% relative to January of 2013 and, therefore, the statement of the Chair of the Committee on Budget and Finance proves to be accurate.

As for the exchange rate of the TRY (Turkish lira) against the USD, throughout the last months it has invariably been depreciating in value. In October of 2013, the TRY fell by 10.05% as compared to the same period of 2012, in November – by 12.91%, in December – by 15.65% and in January – by 25.47%. Calculating the average indicator for the fourth quarter of 2013 and January of 2014, we see that the TRY depreciated by 16.02% in the given period. Accordingly, Davit Onoprishvili’s statement regarding a 25% depreciation of the TRY over the span of the last months is inaccurate. Similar to the previous case discussed above, however, in the event of taking into consideration only the month of January, the MP’s statement proves to be correct.

In parallel to the currency depreciations in Turkey and Georgia, the value of the RUB (Russian rouble) saw a decline as well. Specifically, in October 2013 depreciation amounted to 3.02%, in November – 4.20%, in December – 6.97% and in January – 11.61%. Calculating the average indicator for the fourth quarter of 2013 and the month of January of 2014, we get the result of 6.45%. Hence, Davit Onoprishvili’s statement with regard to a 10% depreciation in the value of the RUB is incorrect. Nonetheless, examining the indicator for the month of January, separately, we again come to the conclusion that the MP’s estimations are accurate.

Let us examine Georgia’s import indices in respect to the neighbouring countries.

Table 2. Georgia’s Import Indices (from Russia and Turkey)

Source: The National Bank of Georgia – nbg.ge; x-rates.com

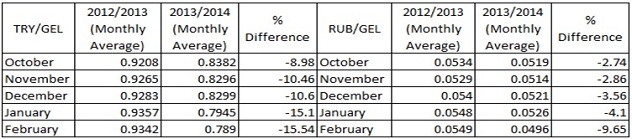

As shown in Table 3, the GEL has been strengthening over the last months with respect to the TRY as well as to the RUB. In October of 2013, the GEL strengthened by 8.98% against the TRY as compared to the same period of 2012 whereas in respect to the RUB, the GEL gained in value by 2.74%. As concerns the subsequent months, the GEL strengthened even further with respect to the aforementioned two currencies.

When a country’s currency is depreciating, exported goods from this country become less expensive for foreigners while for the local inhabitants imported products from foreign countries grow more expensive. The reason for this interrelationship is the fact that with the depreciated currency, local inhabitants have to pay more for each item of imported goods. As concerns the strengthening of the local currency, it produces reverse consequences. Foreigners start paying more for the goods exported from the given country whereas the local inhabitants start paying less for the goods imported from abroad. For instance, given the exchange rate of the EUR/GEL which equals 1:2 and we pay GEL 10 for imported goods worth EUR 5, in the event of the depreciation of the GEL (ex. 1:3), we will have to pay GEL 15 for the same value of products (EUR 5).

As can be surmised, during the devaluation of our currency imported goods become more expensive for us while the products exported from our country become less expensive for foreigners (in the case of the exchange rate of 1:2, foreigners will pay EUR 2.5 for GEL 5 worth of products whereas in the case of the rate of 1:3, they will pay EUR 1.7). As for the strengthening of our currency, if the exchange rate reaches 1:1, we will pay GEL 5 for products with a value of EUR 5 and foreigners will equally pay EUR 5 for GEL 5 worth of goods. Therefore, the strengthening of the GEL renders imported goods less expensive for the Georgian population and makes Georgia’s exported goods more expensive for foreigners. As Turkey and Russia are indeed major importers in Georgia, naturally, the strengthening of the GEL with respect to their currencies would spur an increase in the imports of Georgia and a decrease in exports of the country. This development would fuel a further deterioration of the trade balance.

Obviously, the process described above does not automatically entail that the depreciation of the currency undoubtedly has a favourable impact upon the state economy. Devaluation of the currency can kindle positive repercussions only in specific situations and specific periods of time. In order to determine the actual impact of a currency devaluation on the state economy, we need to be familiar with certain economic parameters of the given country; for example, whether or not the given country can be described as an importer or an exporter (e.g., Georgia is an importing country as over the course of many years imports exceeds the exports of the country), how the depreciation of the currency is reflected upon the volume of imported and exported goods (to what extent it is increasing the exports and decreasing the imports) and, respectively, how does it alter the incomes accrued through these activities. Procurement of such information demands additional and more comprehensive research. Supposing that the depreciation of the currency does indeed boost the incomes of the country, even in that case this process can be advisable only during a certain period of time. The continual devaluation of the currency is prone to spur numerous adverse consequences such as an unstable economic situation in the country, a decline in investments, economic stagnation and so forth.

Table 4. External Trade Indices (USD mln)

Source: The National Bank of Georgia – nbg.ge; x-rates.com

As shown in Table 3, the GEL has been strengthening over the last months with respect to the TRY as well as to the RUB. In October of 2013, the GEL strengthened by 8.98% against the TRY as compared to the same period of 2012 whereas in respect to the RUB, the GEL gained in value by 2.74%. As concerns the subsequent months, the GEL strengthened even further with respect to the aforementioned two currencies.

When a country’s currency is depreciating, exported goods from this country become less expensive for foreigners while for the local inhabitants imported products from foreign countries grow more expensive. The reason for this interrelationship is the fact that with the depreciated currency, local inhabitants have to pay more for each item of imported goods. As concerns the strengthening of the local currency, it produces reverse consequences. Foreigners start paying more for the goods exported from the given country whereas the local inhabitants start paying less for the goods imported from abroad. For instance, given the exchange rate of the EUR/GEL which equals 1:2 and we pay GEL 10 for imported goods worth EUR 5, in the event of the depreciation of the GEL (ex. 1:3), we will have to pay GEL 15 for the same value of products (EUR 5).

As can be surmised, during the devaluation of our currency imported goods become more expensive for us while the products exported from our country become less expensive for foreigners (in the case of the exchange rate of 1:2, foreigners will pay EUR 2.5 for GEL 5 worth of products whereas in the case of the rate of 1:3, they will pay EUR 1.7). As for the strengthening of our currency, if the exchange rate reaches 1:1, we will pay GEL 5 for products with a value of EUR 5 and foreigners will equally pay EUR 5 for GEL 5 worth of goods. Therefore, the strengthening of the GEL renders imported goods less expensive for the Georgian population and makes Georgia’s exported goods more expensive for foreigners. As Turkey and Russia are indeed major importers in Georgia, naturally, the strengthening of the GEL with respect to their currencies would spur an increase in the imports of Georgia and a decrease in exports of the country. This development would fuel a further deterioration of the trade balance.

Obviously, the process described above does not automatically entail that the depreciation of the currency undoubtedly has a favourable impact upon the state economy. Devaluation of the currency can kindle positive repercussions only in specific situations and specific periods of time. In order to determine the actual impact of a currency devaluation on the state economy, we need to be familiar with certain economic parameters of the given country; for example, whether or not the given country can be described as an importer or an exporter (e.g., Georgia is an importing country as over the course of many years imports exceeds the exports of the country), how the depreciation of the currency is reflected upon the volume of imported and exported goods (to what extent it is increasing the exports and decreasing the imports) and, respectively, how does it alter the incomes accrued through these activities. Procurement of such information demands additional and more comprehensive research. Supposing that the depreciation of the currency does indeed boost the incomes of the country, even in that case this process can be advisable only during a certain period of time. The continual devaluation of the currency is prone to spur numerous adverse consequences such as an unstable economic situation in the country, a decline in investments, economic stagnation and so forth.

Table 4. External Trade Indices (USD mln)

Source: National Statistics Office of Georgia – geostat.ge

As can be gathered from Table 4, over the period of 2007-2013 the export volume of Georgia indeed reached an unprecedentedly high indicator (USD 2,909 mln) in 2013 (in line with the preliminary data). It is also to be noted, however, that the largest volume of imported goods was registered in 2013 as well (in line with preliminary data – USD 7,874 mln). Consequently, an “unprecedentedly” high volume of export does not result in an “unprecedented” improvement of foreign trade as the imports and, therefore, a negative trade balance accordingly remain high. The balance of trade has been negative in Georgia throughout the whole period from 2007 to today. During the years 2007-2009 the negative trade balance was characterised with continual fluctuations and from 2009 to 2013 it reveals a tendency of growth. Even though the balance of trade in 2013 (USD -4,965 mln) decreases relative to that of 2012, it is still negative and represents one of the highest indicators witnessed over the course of the last years. As for January of 2014, in this period trade turnover totalled USD 761 million which exceeds the indicator recorded in January of the past year by 15%. Of this amount, export amounted to USD 224 mln (14% more) while import totals USD 538 mln (15% more). As to what concerns the foreign trade balance, it is still negative in January of 2014 and equals USD -314 mln. As can be seen, the negative trade balance has indeed decreased in 2013 relative to the indicator of 2012, precisely as asserted by Davit Onoprishvili. Additionally, granted that Onoprishvili was describing the whole process as positive and not the trade balance itself, this part of the MP’s statement is entirely accurate. If we interpret this part of his statement literally (which, in our opinion, is less probable) assuming that he characterised the balance of trade as positive and not the process on the whole, then this statement is unquestionably false and demagogic.

Conclusion

Our inquiry about the accuracy of Davit Onoprishvili’s statement revealed that on 5 February 2014 the USD/GEL exchange rate equalled 1.7810 (as of 9 April – 1.7495). In line with the data of 2013 the rate of inflation (CPI) amounted to 2.4% (setting the indicator of December against the same period of the previous year) whereas in January 2014 the rate stood at 2.9% (relative to the same month of the previous year). For the year 2014 the monetary policy of the National Bank of Georgia envisages the upper limit of the inflation rate at 6% and so the current rate of inflation is within the defined margins.

Based upon the average indicators of the fourth quarter of 2013 and January of 2014, the GEL depreciated by 2.63% with respect to the USD whereas in January, in particular, the rate of depreciation equalled 6.05%. As regards the TRY and the RUB with respect to the USD, in the fourth quarter of 2013 and January of 2014, the TRY depreciated in value by an average of 16.02% and the RUB – by 6.45%, however in January alone the TRY devalued by 25.47% while the RUB – by 11.61%. As for the exchange rate of the GEL against the TRY and the RUB, in the last months the GEL has strengthened with respect to these currencies.

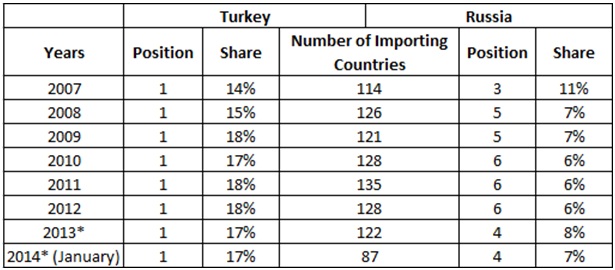

In accordance with the statistical data, Turkey and Russia represent the largest importers in Georgia. As the appreciation of the state currency results in less expensive imported goods for the local population and more expensive exported goods for foreigners, strengthening the GEL against the TRY and the RUB leads to increased imports and decreased exports which creates the deterioration of the trade balance. However, the judgement about the specific impact of a strong currency upon the economy demands additional and more comprehensive research. The negative balance of trade improved in 2013 as compared to 2012 although it still represents one of the highest indicators registered over the course of the past years.

Bearing in mind the facts elaborated in the article, FactCheck concludes that Davit Onoprishvili’s statement: “The exchange rate has practically stabilised now, hovering between 1.77-1.78. The inflation rate is within the established margins. As specified in the State Budget of Georgia, it is not to exceed 6% within a year. I would also like to note that the GEL is not the only currency experiencing a certain decline. Over the course of the last months, the GEL fell by up to 6%. Meanwhile in neighbouring Turkey, the Turkish lira is falling by around 25% and the rate of decline is fairly high in Russia as well; namely, over 10%. These are the major importers in Georgia and, therefore, the strengthening of our currency at this stage would have more detrimental repercussions. The trade parameters took a marked upturn: the growth of [Georgian] export is unprecedentedly high which means that significant changes are underway in this respect, trade balance has decreased and it is positive,” is MOSTLY TRUE.

Originally published in The Financial, issue N. 15(395)

Source: National Statistics Office of Georgia – geostat.ge

As can be gathered from Table 4, over the period of 2007-2013 the export volume of Georgia indeed reached an unprecedentedly high indicator (USD 2,909 mln) in 2013 (in line with the preliminary data). It is also to be noted, however, that the largest volume of imported goods was registered in 2013 as well (in line with preliminary data – USD 7,874 mln). Consequently, an “unprecedentedly” high volume of export does not result in an “unprecedented” improvement of foreign trade as the imports and, therefore, a negative trade balance accordingly remain high. The balance of trade has been negative in Georgia throughout the whole period from 2007 to today. During the years 2007-2009 the negative trade balance was characterised with continual fluctuations and from 2009 to 2013 it reveals a tendency of growth. Even though the balance of trade in 2013 (USD -4,965 mln) decreases relative to that of 2012, it is still negative and represents one of the highest indicators witnessed over the course of the last years. As for January of 2014, in this period trade turnover totalled USD 761 million which exceeds the indicator recorded in January of the past year by 15%. Of this amount, export amounted to USD 224 mln (14% more) while import totals USD 538 mln (15% more). As to what concerns the foreign trade balance, it is still negative in January of 2014 and equals USD -314 mln. As can be seen, the negative trade balance has indeed decreased in 2013 relative to the indicator of 2012, precisely as asserted by Davit Onoprishvili. Additionally, granted that Onoprishvili was describing the whole process as positive and not the trade balance itself, this part of the MP’s statement is entirely accurate. If we interpret this part of his statement literally (which, in our opinion, is less probable) assuming that he characterised the balance of trade as positive and not the process on the whole, then this statement is unquestionably false and demagogic.

Conclusion

Our inquiry about the accuracy of Davit Onoprishvili’s statement revealed that on 5 February 2014 the USD/GEL exchange rate equalled 1.7810 (as of 9 April – 1.7495). In line with the data of 2013 the rate of inflation (CPI) amounted to 2.4% (setting the indicator of December against the same period of the previous year) whereas in January 2014 the rate stood at 2.9% (relative to the same month of the previous year). For the year 2014 the monetary policy of the National Bank of Georgia envisages the upper limit of the inflation rate at 6% and so the current rate of inflation is within the defined margins.

Based upon the average indicators of the fourth quarter of 2013 and January of 2014, the GEL depreciated by 2.63% with respect to the USD whereas in January, in particular, the rate of depreciation equalled 6.05%. As regards the TRY and the RUB with respect to the USD, in the fourth quarter of 2013 and January of 2014, the TRY depreciated in value by an average of 16.02% and the RUB – by 6.45%, however in January alone the TRY devalued by 25.47% while the RUB – by 11.61%. As for the exchange rate of the GEL against the TRY and the RUB, in the last months the GEL has strengthened with respect to these currencies.

In accordance with the statistical data, Turkey and Russia represent the largest importers in Georgia. As the appreciation of the state currency results in less expensive imported goods for the local population and more expensive exported goods for foreigners, strengthening the GEL against the TRY and the RUB leads to increased imports and decreased exports which creates the deterioration of the trade balance. However, the judgement about the specific impact of a strong currency upon the economy demands additional and more comprehensive research. The negative balance of trade improved in 2013 as compared to 2012 although it still represents one of the highest indicators registered over the course of the past years.

Bearing in mind the facts elaborated in the article, FactCheck concludes that Davit Onoprishvili’s statement: “The exchange rate has practically stabilised now, hovering between 1.77-1.78. The inflation rate is within the established margins. As specified in the State Budget of Georgia, it is not to exceed 6% within a year. I would also like to note that the GEL is not the only currency experiencing a certain decline. Over the course of the last months, the GEL fell by up to 6%. Meanwhile in neighbouring Turkey, the Turkish lira is falling by around 25% and the rate of decline is fairly high in Russia as well; namely, over 10%. These are the major importers in Georgia and, therefore, the strengthening of our currency at this stage would have more detrimental repercussions. The trade parameters took a marked upturn: the growth of [Georgian] export is unprecedentedly high which means that significant changes are underway in this respect, trade balance has decreased and it is positive,” is MOSTLY TRUE.

Originally published in The Financial, issue N. 15(395)

Source: National Bank of Georgia – nbg.ge; x-rates.com

As can be seen in Table 1, over the course of the last five months (as compared to the same period of the past year) the GEL was depreciating with respect to the USD. In October of 2013, the value of the GEL fell by 0.32%, in November – by 0.96%, in December – by 3.19% and in January – by 6.05% (as compared to the same months of the previous year). Calculation of the average indicator for the given period reveals that on the whole, over the months of October, November, December and January, the GEL depreciated by 2.63%. This figure does not correspond to the number indicated in the statement of Davit Onoprishvili (claiming a 6% depreciation of the GEL over the course of the last months). However, if we take into account the indicator for January, separately, we observe that the GEL depreciated by 6.05% relative to January of 2013 and, therefore, the statement of the Chair of the Committee on Budget and Finance proves to be accurate.

As for the exchange rate of the TRY (Turkish lira) against the USD, throughout the last months it has invariably been depreciating in value. In October of 2013, the TRY fell by 10.05% as compared to the same period of 2012, in November – by 12.91%, in December – by 15.65% and in January – by 25.47%. Calculating the average indicator for the fourth quarter of 2013 and January of 2014, we see that the TRY depreciated by 16.02% in the given period. Accordingly, Davit Onoprishvili’s statement regarding a 25% depreciation of the TRY over the span of the last months is inaccurate. Similar to the previous case discussed above, however, in the event of taking into consideration only the month of January, the MP’s statement proves to be correct.

In parallel to the currency depreciations in Turkey and Georgia, the value of the RUB (Russian rouble) saw a decline as well. Specifically, in October 2013 depreciation amounted to 3.02%, in November – 4.20%, in December – 6.97% and in January – 11.61%. Calculating the average indicator for the fourth quarter of 2013 and the month of January of 2014, we get the result of 6.45%. Hence, Davit Onoprishvili’s statement with regard to a 10% depreciation in the value of the RUB is incorrect. Nonetheless, examining the indicator for the month of January, separately, we again come to the conclusion that the MP’s estimations are accurate.

Let us examine Georgia’s import indices in respect to the neighbouring countries.

Table 2. Georgia’s Import Indices (from Russia and Turkey)

Source: The National Bank of Georgia – nbg.ge; x-rates.com

As shown in Table 3, the GEL has been strengthening over the last months with respect to the TRY as well as to the RUB. In October of 2013, the GEL strengthened by 8.98% against the TRY as compared to the same period of 2012 whereas in respect to the RUB, the GEL gained in value by 2.74%. As concerns the subsequent months, the GEL strengthened even further with respect to the aforementioned two currencies.

When a country’s currency is depreciating, exported goods from this country become less expensive for foreigners while for the local inhabitants imported products from foreign countries grow more expensive. The reason for this interrelationship is the fact that with the depreciated currency, local inhabitants have to pay more for each item of imported goods. As concerns the strengthening of the local currency, it produces reverse consequences. Foreigners start paying more for the goods exported from the given country whereas the local inhabitants start paying less for the goods imported from abroad. For instance, given the exchange rate of the EUR/GEL which equals 1:2 and we pay GEL 10 for imported goods worth EUR 5, in the event of the depreciation of the GEL (ex. 1:3), we will have to pay GEL 15 for the same value of products (EUR 5).

As can be surmised, during the devaluation of our currency imported goods become more expensive for us while the products exported from our country become less expensive for foreigners (in the case of the exchange rate of 1:2, foreigners will pay EUR 2.5 for GEL 5 worth of products whereas in the case of the rate of 1:3, they will pay EUR 1.7). As for the strengthening of our currency, if the exchange rate reaches 1:1, we will pay GEL 5 for products with a value of EUR 5 and foreigners will equally pay EUR 5 for GEL 5 worth of goods. Therefore, the strengthening of the GEL renders imported goods less expensive for the Georgian population and makes Georgia’s exported goods more expensive for foreigners. As Turkey and Russia are indeed major importers in Georgia, naturally, the strengthening of the GEL with respect to their currencies would spur an increase in the imports of Georgia and a decrease in exports of the country. This development would fuel a further deterioration of the trade balance.

Obviously, the process described above does not automatically entail that the depreciation of the currency undoubtedly has a favourable impact upon the state economy. Devaluation of the currency can kindle positive repercussions only in specific situations and specific periods of time. In order to determine the actual impact of a currency devaluation on the state economy, we need to be familiar with certain economic parameters of the given country; for example, whether or not the given country can be described as an importer or an exporter (e.g., Georgia is an importing country as over the course of many years imports exceeds the exports of the country), how the depreciation of the currency is reflected upon the volume of imported and exported goods (to what extent it is increasing the exports and decreasing the imports) and, respectively, how does it alter the incomes accrued through these activities. Procurement of such information demands additional and more comprehensive research. Supposing that the depreciation of the currency does indeed boost the incomes of the country, even in that case this process can be advisable only during a certain period of time. The continual devaluation of the currency is prone to spur numerous adverse consequences such as an unstable economic situation in the country, a decline in investments, economic stagnation and so forth.

Table 4. External Trade Indices (USD mln)

Source: National Statistics Office of Georgia – geostat.ge

As can be gathered from Table 4, over the period of 2007-2013 the export volume of Georgia indeed reached an unprecedentedly high indicator (USD 2,909 mln) in 2013 (in line with the preliminary data). It is also to be noted, however, that the largest volume of imported goods was registered in 2013 as well (in line with preliminary data – USD 7,874 mln). Consequently, an “unprecedentedly” high volume of export does not result in an “unprecedented” improvement of foreign trade as the imports and, therefore, a negative trade balance accordingly remain high. The balance of trade has been negative in Georgia throughout the whole period from 2007 to today. During the years 2007-2009 the negative trade balance was characterised with continual fluctuations and from 2009 to 2013 it reveals a tendency of growth. Even though the balance of trade in 2013 (USD -4,965 mln) decreases relative to that of 2012, it is still negative and represents one of the highest indicators witnessed over the course of the last years. As for January of 2014, in this period trade turnover totalled USD 761 million which exceeds the indicator recorded in January of the past year by 15%. Of this amount, export amounted to USD 224 mln (14% more) while import totals USD 538 mln (15% more). As to what concerns the foreign trade balance, it is still negative in January of 2014 and equals USD -314 mln. As can be seen, the negative trade balance has indeed decreased in 2013 relative to the indicator of 2012, precisely as asserted by Davit Onoprishvili. Additionally, granted that Onoprishvili was describing the whole process as positive and not the trade balance itself, this part of the MP’s statement is entirely accurate. If we interpret this part of his statement literally (which, in our opinion, is less probable) assuming that he characterised the balance of trade as positive and not the process on the whole, then this statement is unquestionably false and demagogic.

Conclusion

Our inquiry about the accuracy of Davit Onoprishvili’s statement revealed that on 5 February 2014 the USD/GEL exchange rate equalled 1.7810 (as of 9 April – 1.7495). In line with the data of 2013 the rate of inflation (CPI) amounted to 2.4% (setting the indicator of December against the same period of the previous year) whereas in January 2014 the rate stood at 2.9% (relative to the same month of the previous year). For the year 2014 the monetary policy of the National Bank of Georgia envisages the upper limit of the inflation rate at 6% and so the current rate of inflation is within the defined margins.

Based upon the average indicators of the fourth quarter of 2013 and January of 2014, the GEL depreciated by 2.63% with respect to the USD whereas in January, in particular, the rate of depreciation equalled 6.05%. As regards the TRY and the RUB with respect to the USD, in the fourth quarter of 2013 and January of 2014, the TRY depreciated in value by an average of 16.02% and the RUB – by 6.45%, however in January alone the TRY devalued by 25.47% while the RUB – by 11.61%. As for the exchange rate of the GEL against the TRY and the RUB, in the last months the GEL has strengthened with respect to these currencies.

In accordance with the statistical data, Turkey and Russia represent the largest importers in Georgia. As the appreciation of the state currency results in less expensive imported goods for the local population and more expensive exported goods for foreigners, strengthening the GEL against the TRY and the RUB leads to increased imports and decreased exports which creates the deterioration of the trade balance. However, the judgement about the specific impact of a strong currency upon the economy demands additional and more comprehensive research. The negative balance of trade improved in 2013 as compared to 2012 although it still represents one of the highest indicators registered over the course of the past years.

Bearing in mind the facts elaborated in the article, FactCheck concludes that Davit Onoprishvili’s statement: “The exchange rate has practically stabilised now, hovering between 1.77-1.78. The inflation rate is within the established margins. As specified in the State Budget of Georgia, it is not to exceed 6% within a year. I would also like to note that the GEL is not the only currency experiencing a certain decline. Over the course of the last months, the GEL fell by up to 6%. Meanwhile in neighbouring Turkey, the Turkish lira is falling by around 25% and the rate of decline is fairly high in Russia as well; namely, over 10%. These are the major importers in Georgia and, therefore, the strengthening of our currency at this stage would have more detrimental repercussions. The trade parameters took a marked upturn: the growth of [Georgian] export is unprecedentedly high which means that significant changes are underway in this respect, trade balance has decreased and it is positive,” is MOSTLY TRUE.

Originally published in The Financial, issue N. 15(395)